The Market Is Booming The Economy Underneath It Is Not. That Is the Signal Most Investors Are Missing.

A concentrated AI and technology rally is masking deeper fragility across 87% of the U.S. economy. Veteran strategist Jim Paulsen calls it "Bust Booming." For allocators, the question is not whether the market keeps rising. It is whether the foundation beneath it can support what has been built on top.

The S&P 500 is up sharply in 2026. The headline number looks strong. But beneath that number, the economy has split into two fundamentally different realities, and the divergence between them is the most consequential signal in capital markets right now.

Jim Paulsen, the former chief strategist at the Leuthold Group, describes the dynamic as "BustBooming." The technology and AI sector, which represents roughly 13% of U.S. GDP, is growing at double digit rates. The remaining 87% of the economy, what Paulsen calls the "old era," is growing at approximately 1% over the last six quarters. That is an uncomfortably sluggish pace that in most environments would prompt immediate policy response.

But policy response is constrained. Inflation jumped to 3.3% in March, driven by the Iran war's impact on energy costs. The odds that the Fed will raise rates by year end rose to 17% last week, up from 0% the week prior. Consumer sentiment is near historic lows. The economy is not in recession in aggregate, but the vast majority of it is operating under conditions that feel recessionary for the households and businesses that live there.

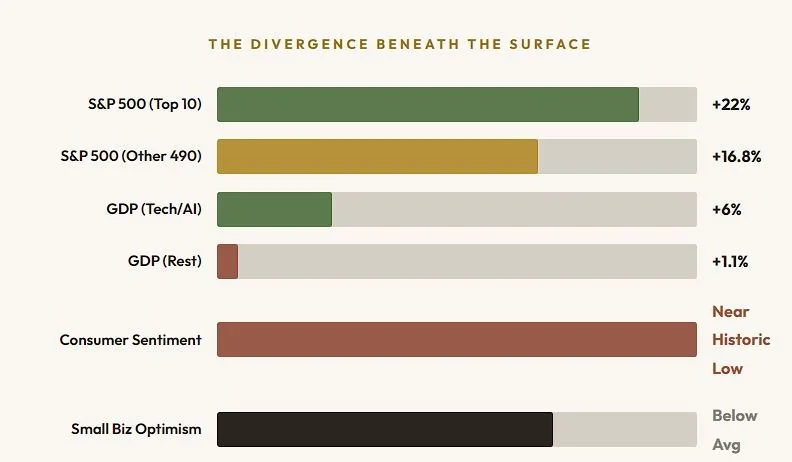

Two Economies Running at Two Speeds

Source: Bloomberg, University of Michigan, NFIB, S&P Dow Jones Indices, Paulsen Perspectives, BEA.

The simplest way to understand this: the stock market and the economy have disconnected. Markets are being carried by a small group of AI and technology companies that are genuinely thriving. But the broader economy, the part where most people work, shop, borrow, and live, is barely growing.

This creates three problems that allocators should be paying attention to.

-

When the S&P 500 rises 13%, it is easy to assume the economy is healthy. But if most of that return comes from 10 stocks, the index is not reflecting economic reality. It is reflecting a narrow AI boom. The top 10 names in the index are up 22%. The other 490 are up 16.8%. The gap is not dramatic yet, but the underlying economic divergence driving it is.

-

The "old era" economy includes housing, healthcare, transportation, food service, and retail. These sectors serve the majority of American households. When they grow at 1%, it means incomes are stagnant, costs are rising, and the financial margin for error is shrinking. This is not a data abstraction. It is the lived experience of roughly 280 million Americans.

-

The Fed cannot cut rates because inflation is elevated at 3.3%. It cannot raise them without further pressuring the 87% of the economy that is already struggling. Rate hike odds jumped from 0% to 17% in a single week. Paulsen is calling for fiscal and monetary support, but political dynamics make that unlikely in the near term. Uncertainty is the operating environment.

What Most Investors See vs. What Is Actually Happening

Paulsen also flags a less followed warning signal. A steepening yield curve has historically been followed by weaker tech sector earnings within 18 months. The curve has steepened significantly since mid 2025. This does not guarantee a decline, but it is a pattern that institutional allocators track carefully because it has preceded every major tech sector correction in the modern era.

Markets that are carried by a narrow set of companies while the broader economy stagnates are markets that are pricing in a future that only 13% of the economy is actually building.

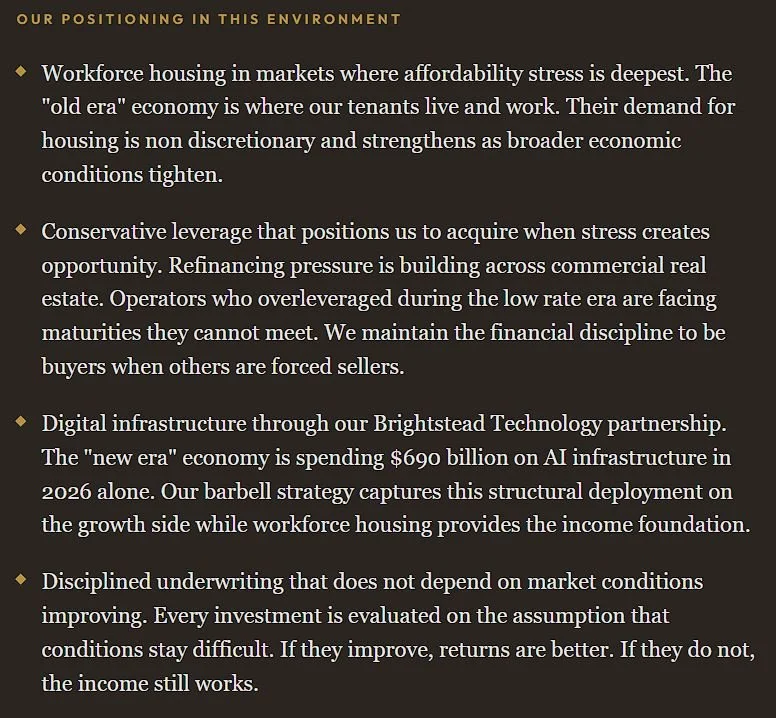

What This Means for Affordable Housing and Real Assets

The "BustBooming" dynamic has a direct and specific implication for real assets, particularly workforce housing.

When 87% of the economy is growing at 1%, the households that live in that economy are under genuine financial pressure. Wages are stagnant relative to costs. Homeownership remains out of reach with mortgage rates above 6%, insurance costs rising, and down payments requiring family wealth. These households are not choosing to rent. They are structurally locked into rental housing by economic conditions that the AI boom has done nothing to change.

That dynamic is why workforce housing demand is not cyclical. It is structural. It does not depend on the economy booming. It persists, and in many ways strengthens, when the economy is struggling. Paulsen's data confirms what we observe at the asset level: the part of the economy where most Americans live is under pressure. That pressure translates directly into durable rental demand, strong renewal rates, and occupancy stability in Class B multifamily housing.

The concentrated rally in AI and technology does not reduce the need for affordable housing. If anything, it widens the gap. The wealth created by the "new era" economy is not distributed to the households who need workforce housing. The pressure on those households is the demand signal.

What We're Doing at Impact Growth Capital

We are not positioning around whether AI stocks rise or fall. We are positioning around the structural reality that Paulsen's data confirms: the vast majority of the U.S. economy is under pressure, and that pressure creates durable demand for the assets we invest in.

Five Signals Allocators Should Track

The U.S. economy has split into two realities. The "new era" (13% of GDP, tech/AI) is booming. The "old era" (87% of GDP) is growing at approximately 1%. Paulsen calls it "BustBooming."

The S&P 500 rally is concentrated, not broad. Markets are reflecting an AI boom, not economic health. Concentrated rallies create blind spots for investors who equate index performance with fundamental strength.

Policy is constrained. The Fed cannot cut (inflation at 3.3%) and cannot raise (87% of the economy is barely growing). Rate hike odds jumped from 0% to 17% in a single week. Uncertainty is the operating environment.

Affordability stress is deepening in the real economy. This directly reinforces workforce housing demand. Households in the old era economy are structurally locked into rental housing by conditions the AI boom has not changed.

Disciplined capital should be positioned in assets where demand is structural and income does not depend on the concentrated rally continuing. Workforce housing, essential infrastructure, and private credit sit in that category.

The Rally Is Real. The Foundation Is Not.

The market is not wrong. AI is genuinely transformative. The capital being deployed is real. But markets that are carried by a narrow set of companies while the broader economy stagnates are markets that are pricing in a future that only 13% of the economy is actually building.

For allocators, the signal is not to short technology or avoid AI exposure. It is to recognize that the concentrated rally has created a blind spot. The 87% of the economy that is barely growing is where most Americans live, work, and rent. That economy generates the demand for workforce housing, essential infrastructure, and the durable income streams that institutional capital is built to compound over decades.

“We do not chase the rally. We position around the structural demand that exists regardless of whether the rally continues. That is the difference between reacting to headlines and allocating to fundamentals.”