This Isn't About Rates. It's About Control of the Federal Reserve.

The rate hold is noise. The governance fracture is the signal. And most allocators are watching the wrong variable.

The Rate Decision Is the Least Interesting Thing That Happened

The Federal Reserve held rates steady at 3.50% to 3.75%. That is the headline. It is also the least consequential piece of information to come out of this meeting.

Markets responded the way markets typically respond. Rate sensitive assets moved. Forward curves adjusted. Commentary focused on timing: when will cuts begin, how many basis points, what does the dot plot suggest. The standard cycle of interpretation played out in real time.

But the standard cycle of interpretation is missing the actual story.

What happened inside the Federal Reserve this month is not a policy event. It is a governance event. The institution responsible for the most consequential monetary decisions on earth is entering a period of structural transition, and the internal mechanics of that transition are far more relevant to capital allocation strategy than whether the next move is 25 basis points up or down.

The rate decision tells you where the Fed is today. The governance shift tells you how it will make decisions for the next several years. One of those matters significantly more than the other.

Powell, the Dissents, and a Fractured Committee

Jerome Powell will step down as Chair but remain on the Board of Governors. This is not a standard playbook. The last time a Fed Chair stayed on as a governor after relinquishing the chairmanship was 1948, when Marriner Eccles did so under Truman. That was a different institution operating in a different economy. The precedent exists, but its relevance to the current moment is limited.

What matters is the dynamic Powell's presence creates. A former Chair sitting on the Board is not a passive actor. It introduces a gravitational pull on committee deliberation, a voice that carries institutional weight even without the title. For Kevin Warsh, who is expected to take the chairmanship with an explicit mandate to reform how the Fed operates, this is a structural constraint built into the committee from day one.

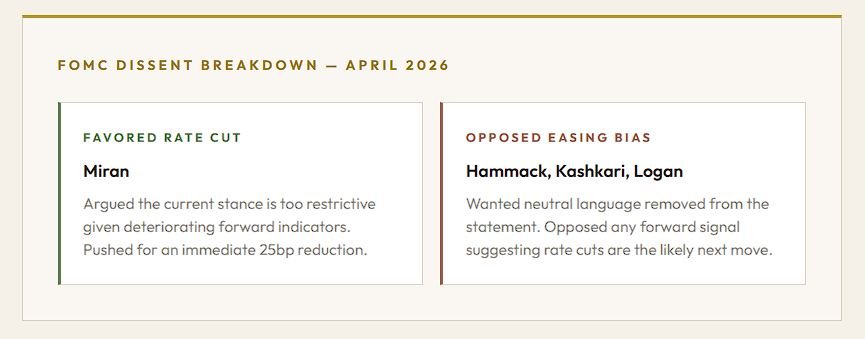

Four dissents on a single decision is the highest count since 1992. But the number alone understates the significance. These dissents did not point in the same direction. One member pushed for a cut. Three others wanted the committee to abandon its easing bias entirely. The committee is not simply disagreeing about timing. It is disagreeing about the framework.

This is the environment Warsh inherits. Not a committee that is cautious but aligned. A committee that is fundamentally split on whether the current policy stance is too tight, too loose, or structurally mischaracterized in the statement language itself.

Warsh has signaled an intent to reshape the Fed's approach: new models, new communication practices, a rethinking of balance sheet strategy. The financial press has described this as regime change. That framing is directionally correct. But regime change requires institutional cooperation, and the committee he is walking into has already demonstrated, publicly, that cooperation is not guaranteed.

The Market Is Solving the Wrong Equation

The dominant market conversation right now is about the path of interest rates in 2026. When will the first cut arrive. How deep will the easing cycle go. What the terminal rate looks like on the other side.

These are not irrelevant questions. But they are the wrong priority.

If the Federal Reserve were operating as a unified institution with a clear consensus on the policy framework, rate forecasting would be a reasonable exercise. You would be modeling a stable decision making process with known variables. But that is not what the data is showing. The data is showing an institution in transition, with unresolved internal disagreements about the analytical framework, the communication strategy, and the balance sheet doctrine.

In that environment, point estimates on the rate path carry less informational value than they normally would. The variance around those estimates is wider. The confidence interval is wider. And the risk of a policy outcome that surprises in either direction is meaningfully elevated.

When the institution itself is unstable, forecasting its output with precision is not analysis. It is guesswork dressed in conviction.

Most institutional investors are still running the standard playbook: position for cuts, model the timing, tilt toward rate sensitive assets. That playbook assumes a stable policy function. The stable policy function is exactly what is breaking down.

It's Not About What They Decide. It's About How They Decide.

The deeper issue is not the rate. It is the decision architecture.

For the past two decades, Fed policy has operated within a broadly stable framework. Inflation targeting at 2%. Forward guidance as a primary communication tool. Balance sheet operations as an extension of rate policy. Regardless of who held the chair, the institutional machinery functioned within known parameters.

Warsh's appointment represents a deliberate departure from that continuity. The mandate is not to fine tune the existing framework. It is to replace meaningful parts of it. New models for assessing economic conditions. A different approach to how the Fed communicates with markets. A reevaluation of how the balance sheet is managed.

Any one of those changes would be significant in isolation. Taken together, they represent a transition in the operating system of American monetary policy. And the four way dissent at this meeting is an early signal that the transition will not be smooth. There are members of the committee who believe the current framework is appropriate. There are others who believe it needs to move in a direction Warsh may not intend.

For allocators, this means the uncertainty is not cyclical. It is structural. It is not about where we are in the rate cycle. It is about whether the rate cycle itself will be governed by the same logic that has been in place for the past 20 years.

Positioning for Governance Risk, Not Rate Risk

When the policy function itself is uncertain, the allocation framework needs to adjust accordingly.

The first adjustment is straightforward: reduce exposure to assets whose performance depends on the precise timing or magnitude of rate movements. If the confidence interval around the rate path is wider than consensus assumes, assets that are priced for a specific sequence of cuts carry more risk than they appear to. Rate sensitive real estate, long duration fixed income, and leveraged structures that rely on refinancing windows are all exposed to this dynamic.

The second adjustment is more fundamental: increase allocation to assets with durable, non discretionary demand that generates cash flow regardless of the rate environment. These are assets where the revenue is structurally embedded, not cyclically dependent.

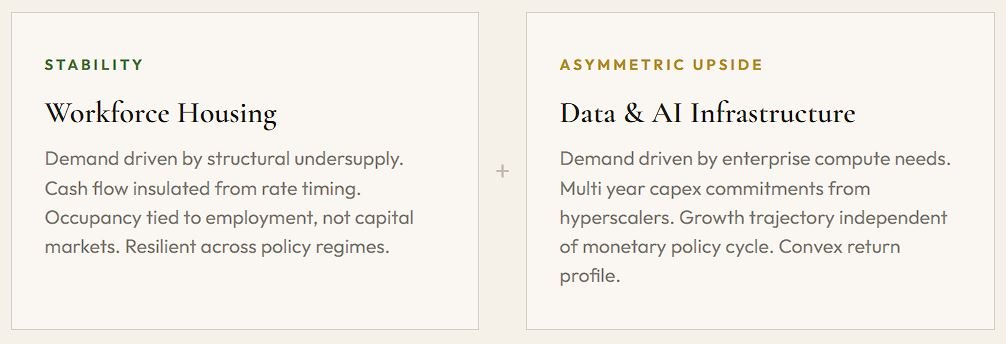

Workforce housing is the clearest example in real estate investing. The demand is driven by chronic undersupply and demographic pressure that operates independently of Federal Reserve policy. Whether rates are at 3.5% or 5%, the shortage of affordable housing in major employment centers does not resolve. The cash flow is tied to occupancy, not to cap rate compression or capital markets sentiment.

Digital infrastructure is the parallel case on the growth side. Data centers, fiber networks, and compute capacity are being driven by structural demand from AI deployment, cloud migration, and enterprise digitization. These are not speculative narratives. They are capital expenditure commitments by the largest technology companies in the world, operating on multi year deployment timelines that are not indexed to the federal funds rate.

The Barbell: Stability and Asymmetric Upside

The institutional investing thesis at Impact Growth Capital is built around a barbell that is specifically designed for environments like this one: high policy uncertainty, structural transition, and a market that is still pricing off the old framework.

One side of the barbell provides durability. Workforce housing generates consistent, occupancy driven income that does not require rate cuts to perform. It is not a bet on the Fed. It is a bet on demographics and housing math that has been moving in one direction for 15 years.

The other side provides optionality. Digital infrastructure is early in a secular buildout cycle. The capital being deployed into AI compute, edge networks, and enterprise cloud is not discretionary spending that retreats when policy tightens. It is strategic investment by companies with the balance sheets to execute regardless of the rate environment.

Together, the barbell is designed to perform in the scenario most allocators are not positioned for: a prolonged period where the Federal Reserve itself is the source of uncertainty, not the resolution of it.

When Even the Fed Lacks Consensus

The conventional allocation framework treats Federal Reserve policy as an input variable: uncertain, yes, but ultimately governed by a stable decision process that can be modeled, forecasted, and positioned around.

That assumption is being tested in a way it has not been tested since the early 1980s. The committee is divided. The incoming chair is working against institutional inertia. The outgoing chair is remaining inside the institution. And the analytical framework that has governed monetary policy for a generation is under explicit review.

This is not a rate call. It is a regime question. And regime questions do not resolve on the timeline that markets prefer.

The question is not: what will the Fed do next? The question is: can the Fed agree on what it should do at all? Position capital for the possibility that the answer, for the foreseeable future, is no.