The Bond Market Is Becoming the Real Policy Maker. And That Changes Where Capital Should Go.

UK 30-year gilt yields hit 5.81% this week, the highest since 1998. Global sovereign borrowing will reach $29 trillion in 2026. The $109 trillion bond market is no longer a passive observer of fiscal policy. It is enforcing discipline that governments are unwilling to impose on themselves.

something happened in the UK bond market this week that deserves more attention than it received. On Monday, the 30-year gilt yield briefly touched 5.81%, the highest since 1998, as speculation over Prime Minister Starmer's future renewed concern about the weakened state of Britain's finances. The 10-year yield climbed above 5.1%, nearing levels not seen since 2008. The pound fell 0.6%. Bank stocks dropped over 3%.

This is not primarily a UK story. It is a signal about how sovereign debt markets are functioning globally. And it connects directly to how every asset class, from real estate to private credit to workforce housing, is being priced.

Bond markets are no longer waiting for governments to discipline themselves. They are doing it for them.

01 — The Scale

Why Bond Markets Are Becoming More Powerful

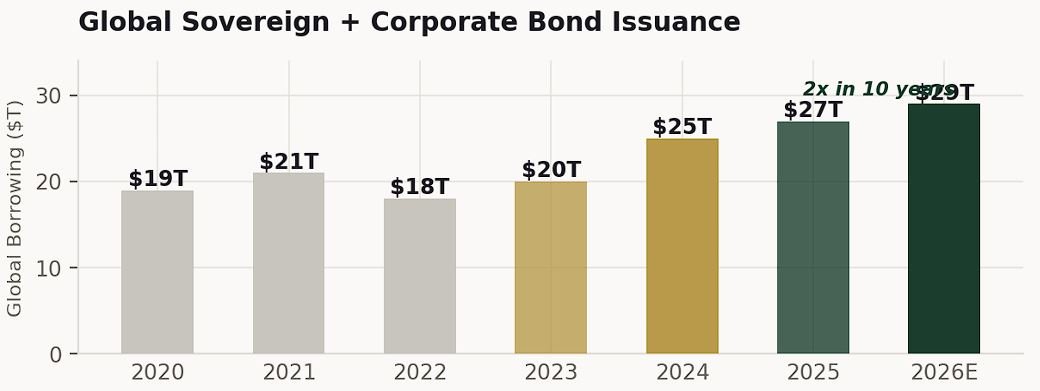

The OECD Global Debt Report 2026 provides the structural context. Governments and corporations are set to borrow $29 trillion from bond markets this year. That is $4 trillion more than 2024 and double the amount from ten years ago. Outstanding sovereign bond debt in OECD countries reached $61 trillion in 2025. The global bond market now stands at $109 trillion, equivalent to 93% of world GDP.

Source: OECD Global Debt Report 2026. Sovereign + corporate issuance. 2026 figure is projection.

At these scales, bond markets are not just financing mechanisms. They are governance mechanisms. When a government's fiscal position weakens, bond investors respond by demanding higher yields. Higher yields mean higher borrowing costs, which means larger interest payments, which means less fiscal flexibility. The cycle is self-reinforcing.

The UK situation this week is the clearest recent example. Political instability combined with unresolved fiscal concerns triggered a repricing that pushed borrowing costs to multi-decade highs in a matter of days. But the OECD data shows this dynamic is not limited to the UK. Debt to GDP rose in 27 of 38 OECD countries in 2025. The ratio is projected to climb to 85% in 2026. Governments everywhere are borrowing more at higher rates, and the market is increasingly sensitive to any signal of fiscal weakness.

02 — The Structural Shift

The Return of Fiscal Discipline

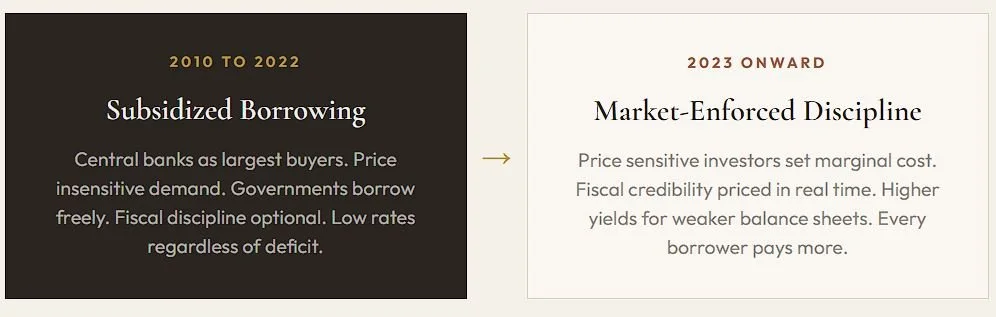

For more than a decade following the financial crisis, bond markets were effectively subsidized by central bank purchases. The Fed, the ECB, and the Bank of England were the largest domestic holders of their own government debt. That purchasing removed price sensitivity from the market. Governments could borrow at low rates regardless of fiscal discipline because the largest buyer was not price sensitive.

That era is over. Central banks have reduced their bond holdings. The OECD reports that the market is now increasingly dependent on price sensitive investors: hedge funds, households, and institutional allocators who demand compensation for risk. When the marginal buyer of government debt is a hedge fund rather than a central bank, fiscal credibility becomes a pricing factor in real time.

The cost of government borrowing is no longer subsidized, and that cost increase ripples across every interest rate in the economy. Mortgage rates, commercial lending rates, private credit pricing, and real estate cap rates are all connected to sovereign yields. When governments pay more, everyone pays more.

03 — The Allocator Signal

The Hidden Signal Beneath Sovereign Debt Stress

For institutional allocators, the sovereign debt repricing creates a specific set of implications that extend well beyond bond portfolios.

-

When the risk free rate rises, every risky asset must offer higher returns to justify deployment. That repricing is happening in real time across real estate, private credit, and growth equity.

-

In a low rate environment, capital flows broadly. In a high rate environment with fiscal uncertainty, capital concentrates in assets with observable cash flows and identifiable collateral. The bar for deployment rises.

-

The OECD reports that 78% of sovereign borrowing in 2026 will be used to refinance existing debt. The same dynamic applies to commercial real estate, where $680 billion in CRE debt matures this year. When refinancing costs are higher, overleveraged borrowers face stress.

-

As traditional bank lending tightens in response to higher sovereign rates and regulatory caution, private credit fills the gap. The structural shift from bank intermediated lending to direct private credit accelerates in exactly this environment. Corporate borrowing reached its highest level ever in real terms in 2025 at $13.7 trillion, with much of that growth flowing through alternative lending channels.

04 — Housing and Private Credit

What This Means for Workforce Housing and Private Credit

The sovereign debt repricing reinforces the thesis for workforce housing and private credit from two directions.

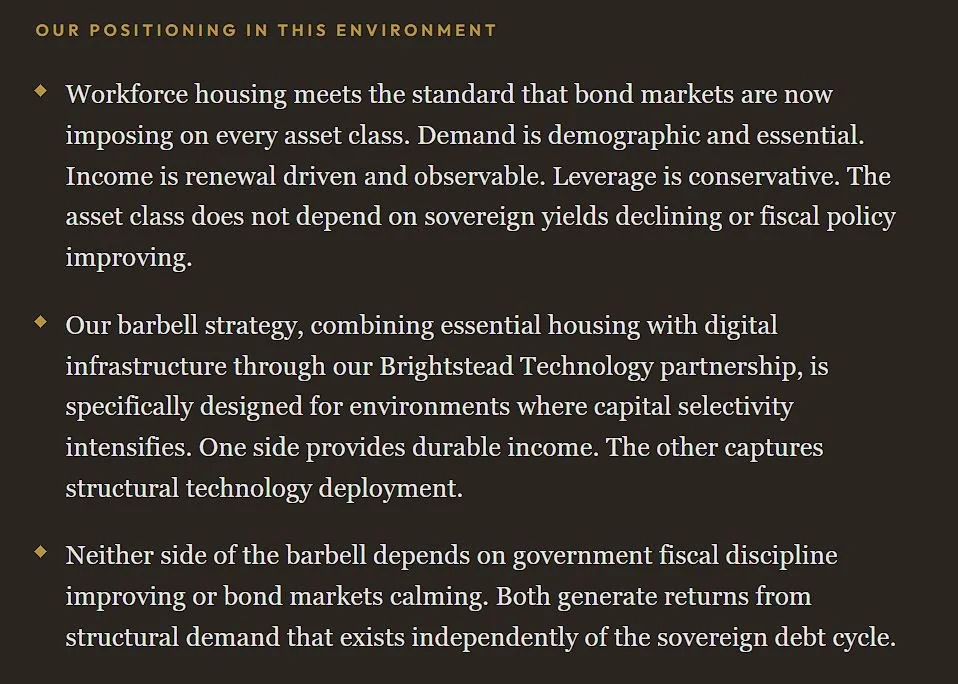

First, higher government borrowing costs keep mortgage rates elevated. When 10-year sovereign yields rise, mortgage rates follow. The path to homeownership moves further away for workforce renters, reinforcing the structural demand floor for Class B multifamily housing. This is not a cyclical effect. It is a transmission mechanism: sovereign fiscal stress directly supports rental demand.

Second, as liquidity becomes more selective, capital concentrates in assets with observable cash flows and real collateral. Workforce housing, with its renewal driven income, demographic demand base, and physical assets, sits precisely in the category where selective capital migrates during periods of uncertainty.

Private credit benefits from the same dynamic. As sovereign yields rise and bank lending tightens, private lenders with capital and discipline capture market share and improved economics.

05 — The IGC Approach

What We Are Doing at Impact Growth Capital

We are not positioning around whether sovereign yields rise or fall. We are positioning around the structural reality that elevated borrowing costs reveal: capital markets are demanding more discipline, more selectivity, and more observable value from every deployment.

06 — Key Themes

Five Signals from the Bond Market

Global sovereign and corporate borrowing will reach $29 trillion in 2026, double the level from ten years ago. The $109 trillion bond market, now 93% of world GDP, is becoming a governance mechanism, not just a financing one.

UK 30-year gilt yields hit 5.81%, the highest since 1998, as political instability exposed fiscal vulnerability. This is a signal, not an isolated event. Debt to GDP rose in 27 of 38 OECD countries in 2025.

Central banks are no longer absorbing supply. Price sensitive investors now set the marginal cost of government borrowing. Fiscal credibility has become a real time pricing factor for the first time in over a decade.

Higher sovereign yields ripple across the entire economy: mortgages, commercial lending, private credit, and real estate cap rates. When governments pay more, every borrower pays more.

Capital migrates toward durable income, real collateral, and essential demand during periods of sovereign stress. Workforce housing, private credit, and essential infrastructure sit directly in that migration path.

Closing Perspective

The Era of Subsidized Borrowing Is Over

Markets no longer assume governments can spend freely without consequences. The era of subsidized borrowing ended when central banks stopped buying. The era of market enforced fiscal discipline has begun. UK gilts this week are the most visible example, but the structural pressure is global.

For allocators, the implication is not to predict where yields go next. It is to recognize that elevated sovereign borrowing costs are structural, not temporary. They reshape the return requirements for every asset class. And they push capital toward assets where the income is observable, the demand is essential, and the return does not depend on fiscal policy improving.

“The bond market is becoming the real policy maker. Sophisticated capital is positioning accordingly.”