The Consumer Is Still Spending. But the Cushion Underneath the Economy Is Getting Thinner.

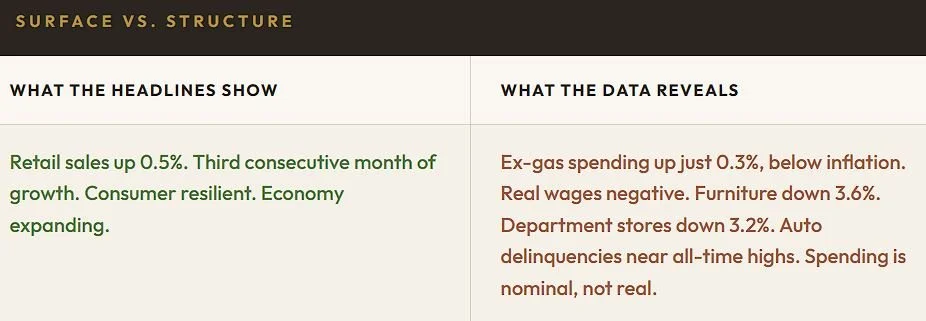

Retail sales rose 0.5% in April. The headline looks fine. Underneath it, Americans are spending more on gasoline and groceries, less on furniture, clothing, and cars. Real wages just turned negative for the first time in three years. The economy is not breaking. But the margin of safety is narrowing in ways that reshape how capital should be positioned.

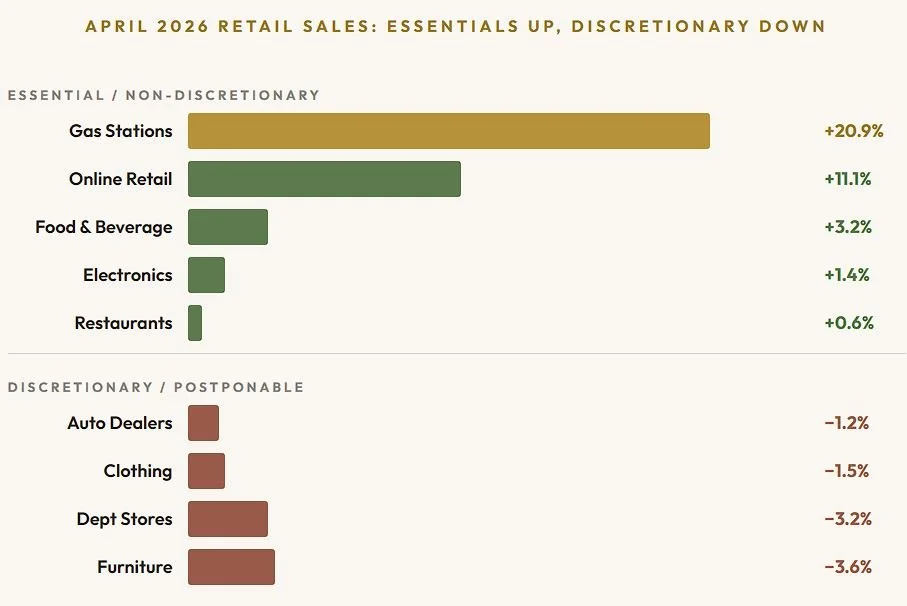

Yesterday's retail sales report showed $757.1 billion in April spending, up 0.5% from March and up 4.9% year over year. At headline level, the consumer looks resilient. Three consecutive months of growth. The economy is spending.

But the composition of that spending tells a very different story. Gasoline station sales surged 20.9% year over year because prices surged, not because Americans are driving more. Food and beverage store sales rose 3.2% because groceries cost more, not because people are eating better. Meanwhile, furniture sales fell 3.6%. Department store sales dropped 3.2%. Clothing was down 1.5%. Auto dealer sales declined 0.5%.

In plain terms: Americans are spending more money on things they cannot avoid and less money on things they can postpone. That is not economic strength. That is economic triage.

Source: U.S. Census Bureau, Advance Monthly Retail Trade Survey, May 14, 2026. Year over year changes.

When you strip out gasoline spending, retail sales grew just 0.3% in April. Against a 0.6% CPI increase, that implies a decline in inflation adjusted consumer spending. The headline resilience is nominal. The real purchasing power story is weakening.

01 — The K-Shaped Economy

One Economy, Two Fundamentally Different Realities

Before we go further, it is worth explaining what a K-shaped economy actually means, because it is one of the most important concepts for understanding where we are right now.

Imagine the letter K. After a shock or a transition, the economy does not recover evenly. The upper arm of the K goes up: wealthier households, higher income earners, and prime borrowers recover quickly. Their assets appreciate, their wages keep pace, and their credit improves. The lower arm of the K goes down: lower income households, hourly workers, and non prime borrowers fall further behind. Their costs rise faster than their incomes, their savings deplete, and their debt burdens grow.

The result is one economy with two fundamentally different lived experiences. The averages look fine because the top pulls the numbers up. But the bottom is under genuine stress that the averages do not capture. That is exactly what is happening in the United States in 2026.

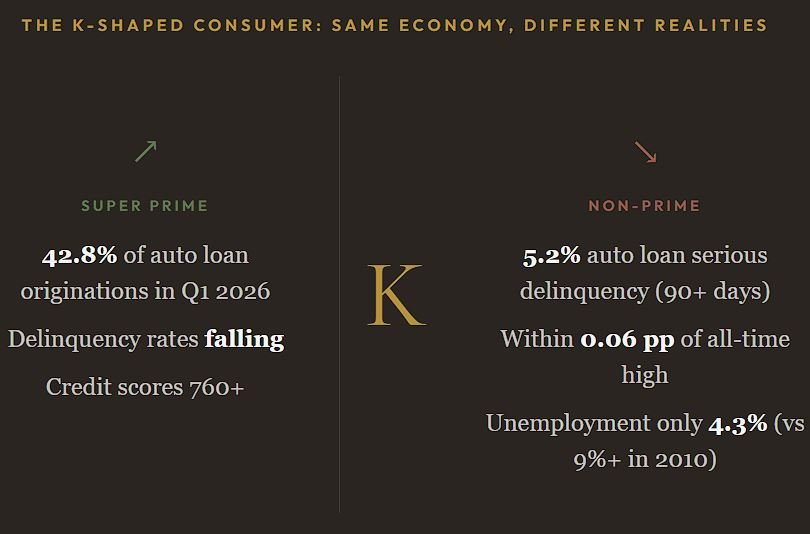

TransUnion's Q1 2026 Credit Industry Insights Report describes a consumer credit market that is increasingly splitting along a K-shaped path, with strength consolidating among super prime consumers and strain rising among non prime households.

The data confirms this across multiple dimensions. Auto loan serious delinquencies (90+ days past due) stand at 5.2%, within 0.06 percentage points of the all-time high set during the financial crisis recovery. The critical context: in 2010, when delinquencies last reached these levels, unemployment was above 9%. Today it is 4.3%. Households are not losing jobs. They are running out of room.

02 — The Purchasing Power Erosion

Why Affordability Pressures Matter for Capital Markets

Real average hourly wages fell 0.3% year over year in April, the first decline since April 2023. Nominal wages grew 3.6%. Inflation ran at 3.8%. The math is simple: paychecks are growing slower than prices. For the first time in three years, working Americans are losing purchasing power.

This has specific implications for capital markets. When real wages turn negative, consumer spending shifts from growth to preservation. Households prioritize rent, food, transportation, and debt payments. Discretionary spending declines. Credit stress increases among lower income borrowers. And the demand for affordable, essential services, including workforce housing, intensifies because the households under pressure have no alternative.

03 — Housing and Private Credit

What This Means for Workforce Housing and Private Lending

The affordability squeeze has a direct and reinforcing effect on workforce housing demand. When real wages are negative, the gap between what households earn and what homeownership costs widens. Mortgage rates above 6%, gasoline at $4.50, insurance costs rising, and now negative real wage growth mean that the path to ownership is moving further away, not closer. Households that were renting by circumstance are increasingly renting by permanent structural constraint.

For workforce housing operators, this translates into stronger occupancy, higher renewal rates, and more durable demand. The tenants in Class B multifamily are not choosing between renting and buying. They are choosing between renewing their lease and facing a housing market that is increasingly unaffordable at every level.

On the credit side, the K-shaped bifurcation is accelerating the shift toward private lending. As banks tighten underwriting for non prime borrowers, private credit fills the gap. The $1.8 trillion private credit market continues to gain share precisely because traditional lending is becoming more selective at a time when more borrowers need capital.

04 — Capital Selectivity

Why Sophisticated Capital Is Becoming More Selective

The April retail data, combined with the inflation trajectory and the K-shaped credit divergence, points to an environment where capital selectivity is not just prudent. It is necessary.

-

Furniture, apparel, and department store spending are declining. Whirlpool reported appliance demand has reached recession level lows. Auto affordability remains strained with more borrowers extending loans to seven years. Consumer facing discretionary sectors are absorbing the purchasing power erosion first.

-

Gasoline, food, housing, and healthcare spending is non discretionary. The consumer is not choosing to spend on these categories. They have no choice. Revenue tied to essential demand does not fluctuate with consumer confidence surveys.

-

Workforce housing, essential infrastructure, and private credit backed by real collateral are the asset classes where the revenue line does not depend on consumer confidence improving. These are the categories where selective capital is concentrating.

05 — The IGC Approach

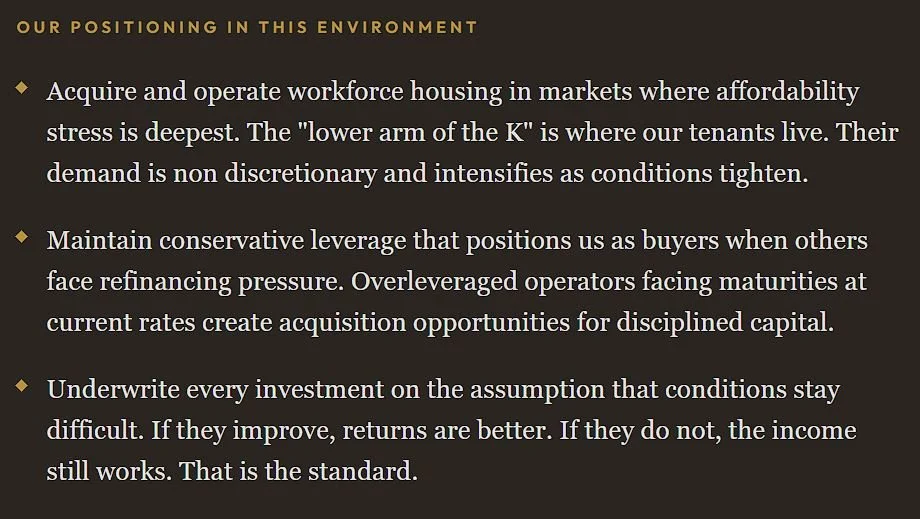

What We're Doing at Impact Growth Capital

The consumer data confirms the environment we have been building for. When real wages turn negative and affordability pressure deepens, the demand for our core asset class, workforce housing, does not weaken. It strengthens.

Our tenants are the households living in the K-shaped economy's lower trajectory. They are employed but squeezed. Their wages are growing but not as fast as their costs. They cannot afford homeownership. They cannot afford to move to a more expensive rental. They renew their leases because the alternative is worse. That is structural demand, and it compounds with every month that affordability pressure persists.

06 — Key Themes

Five Signals from the Consumer Data

Retail sales rose 0.5% in April, but ex-gas spending grew just 0.3%, below inflation. The headline is nominal resilience. The underlying story is real purchasing power erosion.

Real wages turned negative for the first time in three years. Paychecks grew 3.6%. Prices rose 3.8%. The consumer cushion is thinning at the exact moment when costs are accelerating.

The K-shaped economy is deepening. Auto delinquencies at 5.2% are near all-time highs despite 4.3% unemployment. Super prime borrowers are strengthening. Non-prime households are under mounting pressure.

Affordability stress reinforces workforce housing demand. When real wages are negative and homeownership is out of reach, rental demand is not cyclical. It is structural.

Sophisticated capital is becoming more selective: prioritizing essential demand, durable cash flows, and assets where the revenue line does not depend on consumer sentiment improving.

The Cushion Is Getting Thinner. That Is the Signal.

The American consumer is not collapsing. But the financial margin that has supported spending through three years of elevated inflation is narrowing measurably. Real wages just went negative. Discretionary categories are declining. Credit stress is concentrated among the households least able to absorb it. And the Fed, under new leadership, cannot cut rates to relieve the pressure because inflation is accelerating in the wrong direction.

This is not a crisis. It is a transition. And transitions are where disciplined capital separates from reactive capital. The allocators who position in assets tied to essential, structural demand, assets where the income is real and the need does not fluctuate with sentiment, are building portfolios that compound through exactly this kind of environment.

“The consumer is still spending. But the cushion is getting thinner. That is the signal. And it points directly toward the assets we invest in at Impact Growth Capital.”