The Fed Transition May Signal a New Lending Cycle. Sophisticated Capital Is Already Positioning.

Kevin Warsh was confirmed as the 17th Federal Reserve Chair in a 54 to 45 vote, the most divided in modern history. He inherits 3.8% inflation, a divided committee, and a White House expecting rate cuts he may not be able to deliver. The story is not simply about a new chair. The deeper signal is that capital markets may be preparing for a structural transition in lending, liquidity, and institutional deployment.

Something significant happened this week that goes well beyond a personnel change at the Federal Reserve. Kevin Warsh was confirmed as the 17th Chair of the Fed, replacing Jerome Powell in the most partisan confirmation vote for a central bank leader in modern American history. He takes office today, May 16, and will chair his first FOMC meeting on June 16.

For most investors, the headline is about rates: will Warsh cut? When? How fast? But that framing misses the larger signal. What is actually forming beneath the surface is the early architecture of a new lending and investment cycle. And sophisticated capital is already beginning to position for it.

This is not just a leadership change. It may be the beginning of a structural transition in how capital markets function.

Why the Federal Reserve Matters to Every Investor

The Federal Reserve sets the baseline cost of borrowing for the entire economy. When rates are low, capital is cheap: businesses borrow to expand, consumers finance homes and cars, and investors take more risk. When rates are high, the opposite: borrowing slows, asset prices adjust, and capital becomes more selective about where it deploys.

The Fed also controls liquidity, the amount of money flowing through the financial system. Through its balance sheet operations, it can flood markets with capital or drain it. And through its communication, it shapes expectations about the future, which in many ways matters more than the rate itself.

Every investment decision, from a mortgage to a data center to a multifamily acquisition, is made within the framework the Fed creates. When that framework is about to change, the repricing begins before the policy moves. That is what makes this transition so important.

What Warsh Walks Into

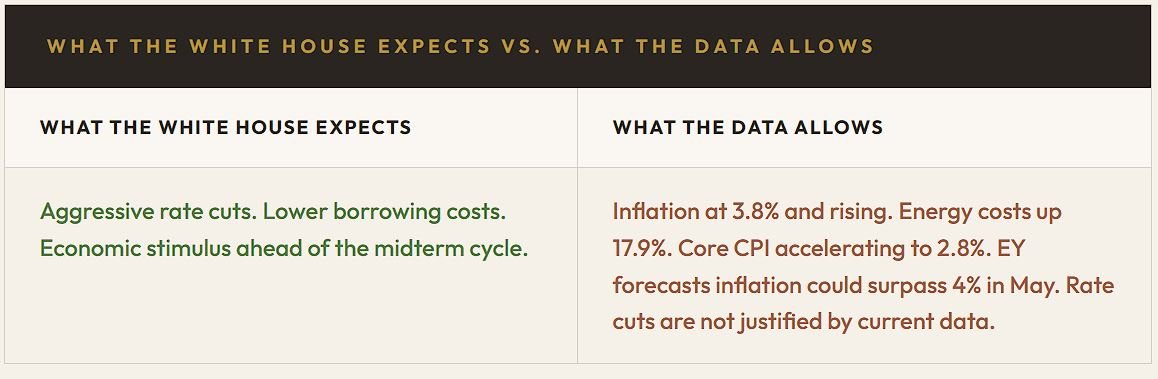

Warsh inherits the most challenging monetary policy environment since at least 2008. Inflation just hit 3.8%, the highest since May 2023, driven by the Iran war's impact on energy costs. Gasoline is averaging $4.50 nationally, up from $3.14 a year ago. Energy costs surged 17.9% year over year. For the first time in three years, wages are no longer outpacing inflation: real average hourly earnings fell 0.3% annually.

At the same time, the committee he inherits is deeply divided. Four members dissented at the April meeting, the most since 1992. Three wanted to remove any easing bias from the statement. One wanted an immediate cut. Markets now price less than 3% probability of any rate cut through December, with hike odds rising through year end.

And Powell is still on the board. For the first time since 1948, a departing Chair has chosen to remain as governor, retaining his FOMC vote. Warsh will need to build consensus with a committee that includes his predecessor, three hawkish regional presidents, and a White House expecting rate cuts he almost certainly cannot deliver in the near term.

The Changes That Actually Matter

Most commentary is focused on when Warsh will cut rates. That is the wrong question. The changes that will reshape capital markets are structural, not cyclical. According to JPMorgan analysts, Warsh has the authority as Chair to implement several significant reforms without needing committee consensus.

-

The Fed currently holds $6.7 trillion in assets, including mortgage backed securities. Warsh has argued this footprint distorts markets and should shrink faster. This has the highest potential to reshape capital flows.

-

Different metrics could change when and how the Fed responds to price pressures. A revised framework would alter the entire calculus for rate expectations.

-

Fewer meetings means less frequent policy signals, which changes how markets price expectations between decisions. Historically, longer gaps between meetings increase deal activity.

-

Less communication means markets have to price in more uncertainty, which changes volatility patterns across every asset class.

-

This could reshape the government bond market and the yield curve, with downstream effects on mortgage rates and real estate financing.

Each of these changes individually would be notable. Together, they represent a potential transformation in how the Federal Reserve interacts with capital markets. And transformation in the policy framework is what creates new lending cycles.

What Most Investors Miss About Fed Transitions

Here is what most investors miss about Fed transitions: the rate decision is the least important part. The most important part is how the transition reshapes expectations, liquidity conditions, and risk appetite across the capital stack.

Major market transitions do not begin with headlines. They begin with shifts in lending expectations, institutional repositioning, and changes in how risk is priced across the capital structure. By the time the headline confirms the transition, the repricing has already occurred. Sophisticated capital moves before the confirmation, not after it.

What we are watching: if Warsh reduces the Fed's balance sheet footprint in mortgage backed securities, it could create temporary pricing dislocations in the mortgage market that benefit private capital. If he reduces meeting frequency, the periods between decisions become longer, which historically increases deal activity as participants stop waiting for the next meeting. If lending conditions stabilize even at current elevated rates, the pent up demand for refinancing, acquisition, and deployment begins to release.

What This Means for Real Estate and Private Markets

The practical implications for real estate and private markets are specific and actionable.

-

Approximately $680 billion in CRE debt matures in 2026. If Warsh signals policy stability, even without cuts, lenders gain confidence in underwriting terms, and refinancing activity accelerates.

-

When the policy path is unclear, traditional bank lending tightens. Private credit fills the gap. The Warsh transition, with its structural uncertainty, reinforces the thesis that private lending continues to gain market share.

-

With inflation at 3.8%, mortgage rates are not coming down. Homeownership remains out of reach for the vast majority of workforce renters. That dynamic is not rate sensitive. It is structural.

-

Markets do not need lower rates to transact. They need clarity. If Warsh provides a stable framework, even at current rate levels, the capital that has been sitting on the sidelines waiting for direction begins to deploy.

What We're Doing at Impact Growth Capital

We do not position capital around rate predictions. We position around structural demand and framework clarity. The Warsh transition reinforces our approach on every dimension.

Five Signals from the Warsh Transition

Warsh was confirmed 54 to 45, the most divided vote for a Fed chair in history. He inherits 3.8% inflation, a committee with four recent dissents, and a predecessor who is staying on the board. This is not a routine transition.

The structural changes Warsh can implement as Chair, including fewer meetings, faster balance sheet reduction, and a new inflation framework, will reshape how capital markets function more than any single rate decision.

Markets price less than 3% probability of a rate cut through December 2026, with hike odds rising. The White House expectation of aggressive easing is unlikely to materialize given current inflation dynamics.

Major market transitions begin quietly through policy shifts, lending expectations, and institutional repositioning. Sophisticated capital moves before the headline fully changes.

Real estate and private markets benefit from framework clarity, not necessarily from rate cuts. If Warsh provides stability at current levels, deal activity, refinancing, and deployment accelerate.

“The next lending cycle will not be announced. It will emerge quietly through shifts in expectations, lending terms, and institutional repositioning. Sophisticated capital does not wait for the announcement. It positions ahead of it.”