Miami Is No Longer a Sun Belt Story. It Is a Global Gateway Story. And the Office Market Proves It.

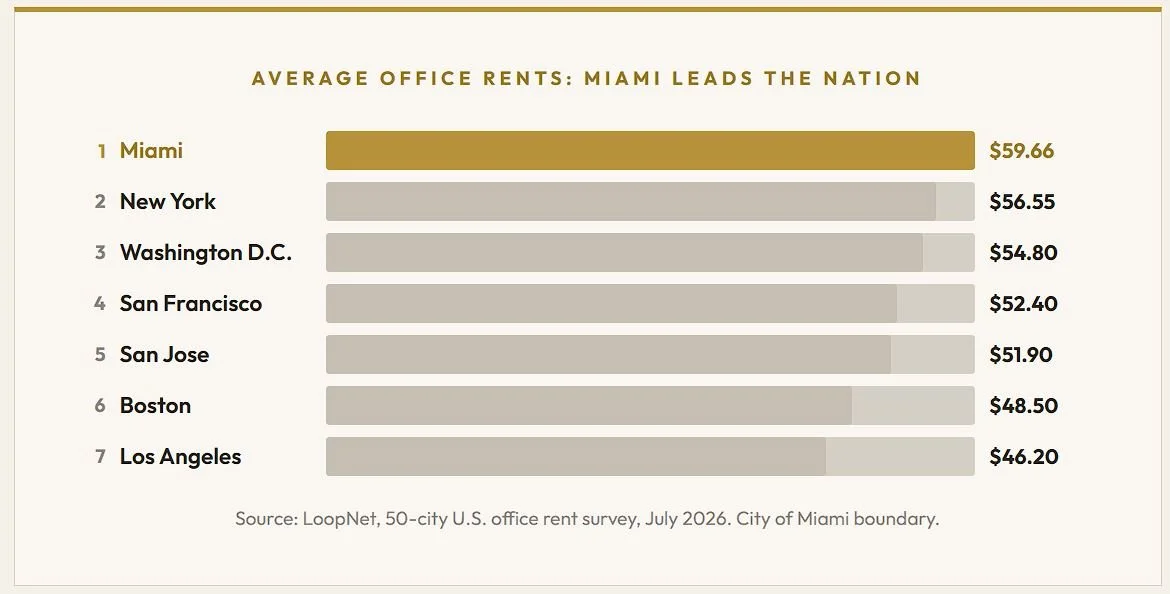

Miami now has the highest office rents in America. Not New York. Not San Francisco. Miami. At $59.66 per square foot, it leads all 50 U.S. cities. Trophy space in Brickell regularly exceeds $100. Peter Thiel just leased at $250. The office market is not dead. It is bifurcating.

Five years ago, the idea that Miami office rents would surpass New York, San Francisco, and Washington D.C. would have been dismissed by most institutional investors. Today it is data, not speculation. And the signal it sends about how capital selects locations, assets, and quality in this cycle is worth examining closely.

Miami Leads All 50 U.S. Cities

LoopNet ranked Miami first among 50 U.S. cities for average office rents at $59.66 per square foot, ahead of New York, Washington D.C., San Francisco, and San Jose. CBRE reports that Brickell Class A rents have grown 74% since 2021 to an average of $102 per square foot. The CBD overall has risen 53% to $76.24. Suburban asking rates climbed 1,100 basis points year over year to $56.89, with Class A suburban reaching $66.23.

At the trophy tier, the numbers are extraordinary. Peter Thiel's family office leased space at 830 Brickell for approximately $250 per square foot, the most expensive office lease in Miami history. Letters of intent have been exchanged at over $200 per square foot at several buildings. Signed deals regularly exceed $150. Citadel's 1.7 million square foot headquarters and Banco Santander's regional office are both under construction in Brickell, adding more Class A inventory to meet demand that is outpacing supply.

Source: CBRE Q4 2025 report, Commercial Observer. Brickell Class A average asking rents.

One data point deserves particular attention: Miami office utilization, at 74.4%, now exceeds Manhattan at 74.1% and far surpasses the national average of 62%. People are not just leasing office space in Miami. They are showing up to it.

Capital, Scarcity, and Institutional Commitment

-

Miami has a relatively small inventory of premium office product compared to traditional gateway cities. When demand surges into a constrained supply, pricing follows. The Brickell, Downtown, and Coconut Grove corridors concentrate most of the high-end inventory.

-

The same capital migration we have tracked across our publications, with $20.6 billion in adjusted gross income flowing into Florida annually, is now materializing as office demand. Wealthy individuals are migrating to South Florida and bringing their money and business with them.

-

Ken Griffin moved Citadel. Paul Singer bought 701 Brickell for $443 million. Apollo CEO Marc Rowan developed boutique office in Miami Beach. Each institutional commitment signals permanence rather than speculation, attracting the next wave of tenants.

-

Companies competing for talent in Miami are leasing amenity-rich, hospitality-style buildings. Developers are responding with private marinas, wellness facilities, and concierge services. The product type that is winning is not commodity office. It is experience-driven workspace.

This is not a story about office recovery. It is a story about asset selection. Weak commodity office in secondary markets and trophy office in Miami are two completely different asset classes trading at completely different economics.

The Office Market Is Not Dead. It Is Bifurcating.

Miami confirms the thesis we have been building across every publication this year: the market is bifurcating, and the advantage belongs to assets where capital, quality, and structural demand overlap.

The office market is splitting into two separate markets. On one side: commodity office in secondary locations with declining demand, rising vacancy, and structural headwinds from remote work. On the other: trophy office in markets where wealth, talent, and institutions are actively concentrating. These two segments are diverging so sharply that averaging their performance together is misleading.

For workforce housing, Miami's office surge reinforces demand from the other direction. As institutional capital, high-income workers, and service businesses follow the relocations into South Florida, the workforce that supports them, from hospitality staff to healthcare workers to construction crews, needs housing they can afford. That demand is structural and deepening.

Four Signals from the Miami Office Market

1. Miami now has the highest average office rents in America at $59.66/SF, ahead of New York, D.C., and San Francisco. Brickell Class A rents grew 74% since 2021 to $102/SF. Trophy leases are reaching $250/SF.

2. The office market is not recovering uniformly. It is bifurcating into two separate asset classes: commodity office under structural pressure and trophy office commanding record pricing in markets where capital concentrates.

3.Miami is becoming less like a typical Sun Belt market and more like a global gateway city, competing not with Austin or Nashville but with New York and London for institutional capital, family offices, and corporate headquarters.

4. The lesson is not that office is back. The lesson is that the best assets in the right markets are still commanding pricing power while the rest of the office market faces structural headwinds.

Which Markets, Which Buildings, Which Tier

Miami is competing with global gateway cities, not just other Sun Belt markets. The premium belongs to scarce, high-quality assets in markets where capital and talent are actively relocating.

“The next decade in commercial real estate will not be defined by whether office recovers. It will be defined by which markets, which buildings, and which asset quality tiers capture the capital that is still very much in motion.”