The Asset Class That Built America.

This weekend, America celebrates 250 years of independence. Before the markets reopen, we step back from the weekly signals and take a longer view. Commercial real estate has not just participated in the American story. It has been the foundation of it.

We spend most of our publications analyzing what is changing: rates, policy, distress, inflation, power constraints, capital flows. This week, ahead of the Fourth of July, we wanted to look at what has not changed: the remarkable, durable, quietly extraordinary performance of commercial real estate as an asset class across the full arc of American economic history.

The headlines rarely celebrate it. Real estate does not have an earnings season. It does not ring an opening bell. It does not surge 30% in a single quarter on AI enthusiasm. But it does something that very few asset classes can claim: it compounds wealth with stock-like returns and bond-like volatility over decades. And it has been doing so for as long as America has existed.

Equity Returns. Fixed Income Stability. Every Decade.

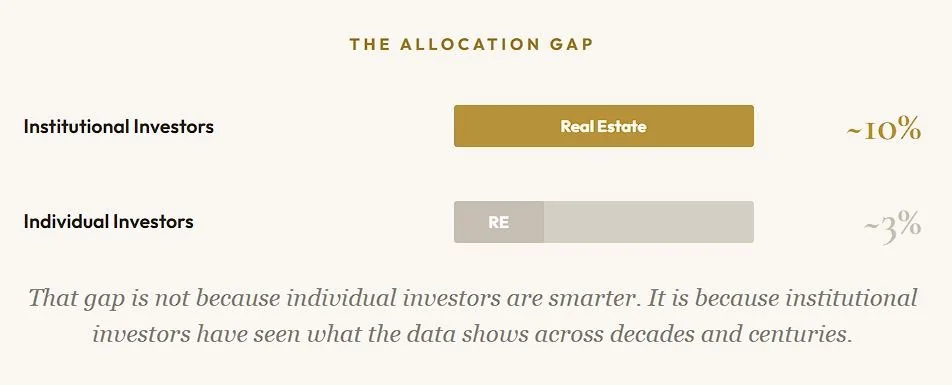

Invesco published an institutional analysis earlier this year showing that U.S. private real estate, measured by the NCREIF Property Index, was either the highest or second highest performing asset class compared to U.S. stocks, bonds, and Treasury yields across every single 10-year rolling period over the past 20 successive periods going back to the mid 1990s. Not some of them. Every one.

Over 25 years, private CRE has returned approximately 10.3% annually. That is competitive with the S&P 500's long-term average of roughly 10%. But here is where it separates: the volatility of CRE returns has been closer to bonds than to stocks. Quarterly price swings in private CRE average about 1.8%, compared to 6.6% for equities.

Sources: NCREIF (NPI), Bloomberg L.P., Damodaran (NYU). 25-year annualized returns and volatility by asset class.

The most counterintuitive finding: real estate delivered equity-like returns with bond-like risk across 145 years and 16 countries. No other asset class occupied that position in the risk-return spectrum.

The Income Floor That Makes It Work

Consider $100,000 invested in January 2000. Over the next 26 years, that investment in private CRE grew with a steadiness that stocks could not match. During 2008, when the S&P 500 fell 37% in a single year, private CRE declined but recovered faster and with less permanent capital destruction. The income component, roughly half of total CRE returns historically, continued generating cash flow even as property values fluctuated.

That income component is the structural advantage. Stocks generate returns primarily through price appreciation and modest dividends (S&P 500 yield: roughly 1.3% in 2024). Real estate generates returns through a dual engine: rental income and property appreciation. REITs delivered a 4.1% dividend yield in 2024 compared to 1.3% for the S&P 500. Private CRE income has averaged even higher. That income floor is what gives real estate its resilience during downturns and its compounding power across full cycles.

Five Structural Advantages

-

Real estate rents and property values tend to rise with inflation. When the cost of building new supply increases, existing assets become more valuable. Unlike bonds, whose real returns erode during inflationary periods, real estate has historically preserved purchasing power across every inflationary cycle in modern history.

-

Private CRE has historically shown low correlation to both stocks and bonds. That means adding real estate to a stock and bond portfolio has improved risk adjusted returns not by increasing returns alone but by reducing portfolio volatility.

-

A 25% down payment on a property that appreciates 5% generates a 20% return on equity. Used conservatively, leverage transforms modest property appreciation into attractive equity returns while the tenant pays down the debt.

-

Depreciation, 1031 exchanges, and capital gains treatment create a tax profile that is structurally more favorable than most asset classes. The effective after-tax return of real estate has historically exceeded its pre-tax advantage over bonds and often narrows the gap with equities.

-

People need places to live, work, shop, receive healthcare, store goods, and process data. That demand does not disappear during recessions. It shifts and adapts, but it does not vanish. Real estate is anchored to the most durable demand in any economy: the physical space that human activity requires.

Every Chapter Written in Real Asset

Westward Expansion

A land story. The foundational economic act of the young republic was the acquisition, distribution, and development of territory.

Industrial Revolution

A factory and warehouse story. Manufacturing wealth was built on physical infrastructure that housed the machines and the workers who ran them.

Post-War Boom

A housing story. The suburban expansion created the largest wealth-building vehicle in American history: homeownership and the communities built around it.

Technology Era

A data center and office story. The digital economy required physical space for servers, campuses, and the infrastructure that connects them.

AI Buildout (Now)

A power infrastructure and digital real estate story. The current chapter is being written in substations, powered land, and the physical layer beneath the algorithms.

At every stage, the allocators who owned the physical foundation beneath the economic narrative, not just the companies riding it, captured durable, compounding wealth that survived the cycles, the crashes, the policy shifts, and the headlines.

That is what we build at IGC. Not the narrative. The foundation.

This Fourth of July, as we celebrate the country that made this asset class possible, I am grateful for the investors who trust us to be disciplined stewards of their capital. The American economy will continue to evolve. The infrastructure it requires, the housing, the warehouses, the data centers, the power, will always be built in real assets. That is where we invest. That is where we will always invest.

Jesse Sells

Co-Founder & COO, Impact Growth Capital