The Fed Held Rates Steady.

But the real story was the shift in expectations.

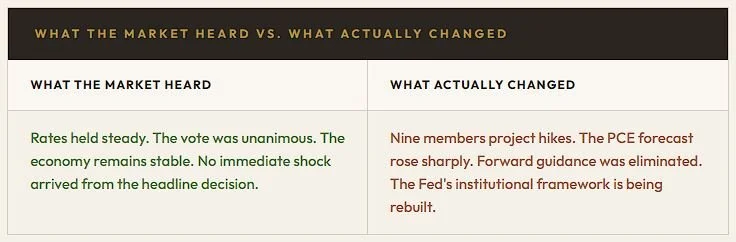

The Federal Reserve left rates unchanged at 3.50% to 3.75% in a unanimous 12-0 vote. On the surface, the decision looked uneventful. Markets expected a hold. The real signal came from everything around the decision: the dot plot, the inflation forecast, the change in communication style, and the new institutional posture under Kevin Warsh.

The rate did not move. The framework did. For investors underwriting real estate, private credit, workforce housing, or infrastructure, that distinction matters more than the headline decision.

Why the Dot Plot Mattered More Than the Rate Decision

A rate decision answers one narrow question: hold or move today. The dot plot reveals how the committee is thinking about tomorrow. That is why this meeting mattered. Nine of eighteen members now expect at least one hike before year-end, and six expect two hikes. Just three months earlier, the median projection still pointed toward cuts.

That is not a small adjustment. It is a change in the market's forward-looking map. Investors who had been underwriting to imminent rate relief now have to consider the opposite: that the next meaningful move may be higher, not lower.

The inflation forecast reinforced the message. The Fed's year-end PCE projection moved from 2.7% to 3.6%, while growth expectations edged lower. That combination leaves policymakers with little room to sound dovish. Inflation is not falling quickly enough, and the economy is not weak enough to justify easy money.

The market focused on the hold. The dot plot is what changed. And when expectations change, every model built around future capital costs has to change with it.

A New Communication Regime Is Emerging

Warsh's first press conference as Fed chair signaled a very different communication style. The post-meeting statement was shorter. Forward guidance was removed. Five task forces were announced to review policy operations, communications, data sources, productivity, labor market interpretation, and inflation drivers.

For over a decade, markets became accustomed to a Fed that helped investors look around the corner. This version appears less interested in providing a predictable path. Warsh's message was clear: the Fed will prioritize price stability, reduce outdated language, and rely more heavily on incoming data than on long-range signaling.

That matters because capital markets do not only price current rates. They price confidence in the path of future rates. If the Fed becomes less predictable by design, investors need wider margins of safety, more conservative exit assumptions, and less dependence on a clean pivot back to cheaper capital.

The Cost of Capital Assumption Has to Be Revisited

The shift in expectations lands directly on commercial real estate. Many refinancing plans, exit strategies, and acquisition models still depend on the idea that rates will normalize lower. This meeting challenged that assumption.

-

If the Fed is signaling possible hikes, investors cannot rely on lower exit cap rates to create returns. The asset has to work on current income, basis, and durable demand.

-

The maturity wall does not become easier if borrowers face the same or higher rates when extensions expire. Extend-and-pretend strategies become increasingly fragile.

-

When mortgage affordability remains constrained, more households stay in the rental market. That supports demand for Class B multifamily and essential, non-discretionary housing.

-

Hyperscaler capital expenditure is driven by compute demand, power constraints, and AI adoption. It is rate-aware, but not rate-dependent in the same way traditional CRE is.

The Next Signals Will Determine Whether Expectations Harden

One meeting does not settle the path of rates. But it changes the burden of proof. The market can no longer assume that a hold is a prelude to cuts. Inflation data, the July meeting, refinancing pressure, and the Fed's task force reviews now carry more weight.

Capital Markets Watchlist

-

May PCE will test whether the Fed's higher inflation forecast becomes the market's new base case.

-

The next FOMC meeting will show whether the committee is willing to move from signaling hikes to actively preparing markets for them.

-

CRE maturities will reveal which borrowers can refinance through higher-for-longer capital and which cannot.

-

Task force recommendations may reshape Fed communication, inflation methodology, and market expectations.

Four Takeaways for Capital Allocators

The Fed held rates steady, but the dot plot shifted sharply. Nine of eighteen members now project hikes before year-end.

Warsh is changing the Fed's posture. Shorter statements, no forward guidance, and institutional reviews point to a less predictable central bank.

Inflation expectations moved higher while growth expectations softened. That creates a more difficult environment for investors waiting on rate relief.

CRE underwriting that depends on cheaper capital needs to be revisited. Durable income, conservative leverage, and essential demand matter more.

The Question Is No Longer Whether Rates Are High

The more important question is whether investors are underwriting a return to cheap capital that may not arrive on schedule, or may not arrive at all. A rate hold can look calm on the surface while the expectations beneath it move violently.

“The Fed did not change the rate. It changed the assumptions investors use to price the future.”