The End of Extend and Pretend. Price Discovery Is Returning to Commercial Real Estate.

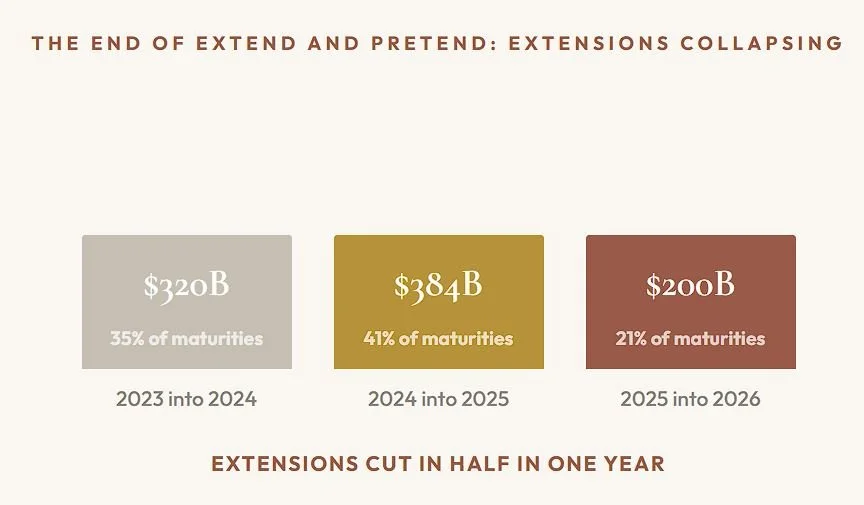

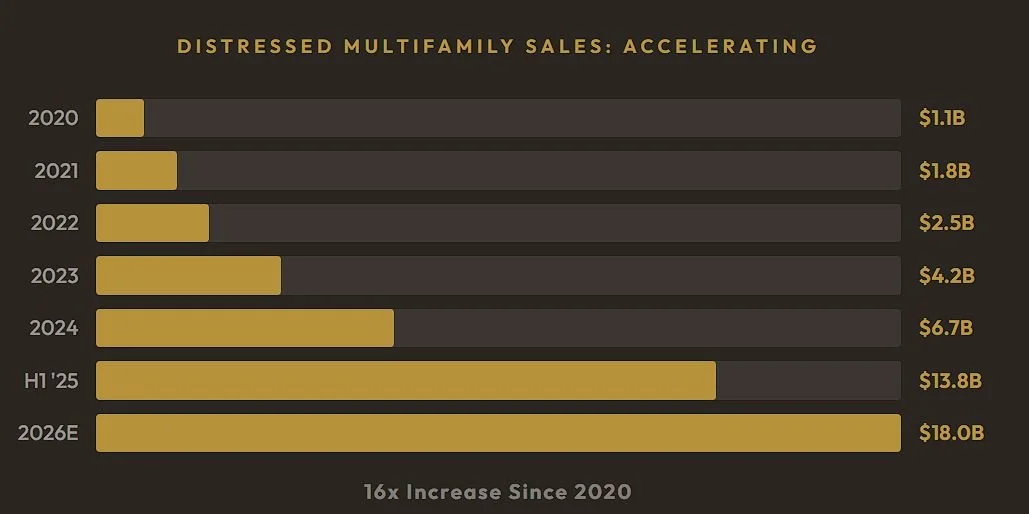

Loan extensions dropped from 41% of maturities to 21% in a single year. Office CMBS delinquencies surpassed 12%. Distressed multifamily sales reached $13.8 billion, a 16x increase since 2020. Lenders are no longer deferring losses. They are resolving them. For disciplined capital, this is not a crisis headline. It is the beginning of the best acquisition environment in over a decade.

For three years, lenders and borrowers have been playing the same game: extend the loan, defer the loss, wait for rate cuts that would make the math work again. It was rational. It was widespread. And it is now ending.

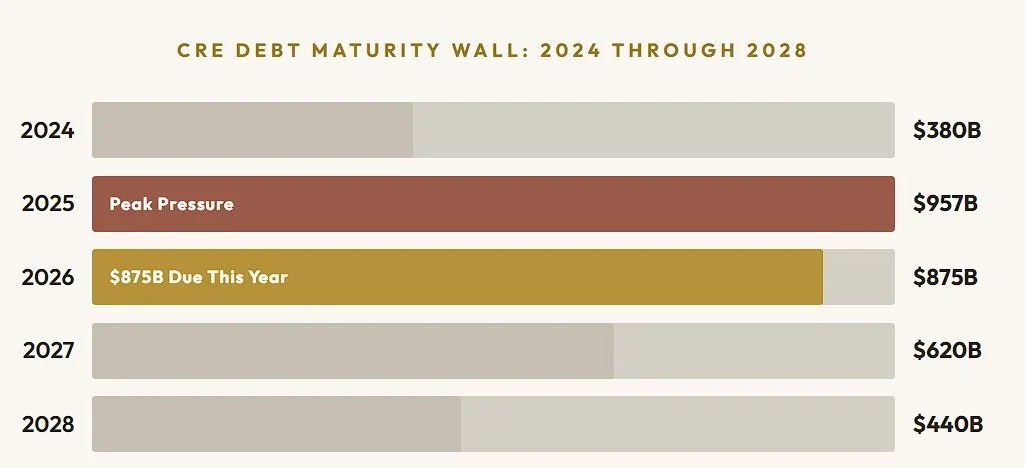

The data is unambiguous. The Mortgage Bankers Association reports $875 billion in commercial mortgages will mature in 2026. Loan extensions, which masked the depth of the problem, collapsed from 41% of maturities in 2024 to 21% in 2025. Lenders are no longer granting time without concessions. They are forcing resolution.

The Economics of Patience Broke Down

For nearly three years, commercial real estate lenders operated under the assumption that time would solve the problem. Extensions delayed recognition of losses while borrowers waited for lower rates, tighter cap rates, and improving valuations to restore refinancing viability.

That assumption is now breaking down. Higher for longer interest rates, persistent inflation, and mounting maturity pressure have fundamentally changed the economics of patience. Carrying distressed loans no longer preserves optionality. It consumes capital, limits new originations, and increases regulatory scrutiny on lender balance sheets.

As a result, the market is beginning to transition from delay to resolution.

Source: First American, Mortgage Bankers Association. Extensions as share of expected maturities at start of each year.

Distressed debt sales, foreclosures, discounted note transactions, and recapitalizations are accelerating across the CRE landscape, particularly in office assets facing structural demand challenges and loans originated at peak valuations during the low rate cycle.

This is not simply a deterioration story. It is a repricing story. And historically, repricing cycles are where sophisticated capital begins positioning for the next recovery phase.

$875 Billion Due in 2026. The Pressure Is Real but Differentiated.

Source: MBA, CRE Daily, Trepp. Includes fixed-rate maturities and floating-rate debt without extension options.

Source: MMG Real Estate Advisors, CoStar. Rolling 12-month distressed multifamily transaction volume.

From Frozen Markets to Price Discovery

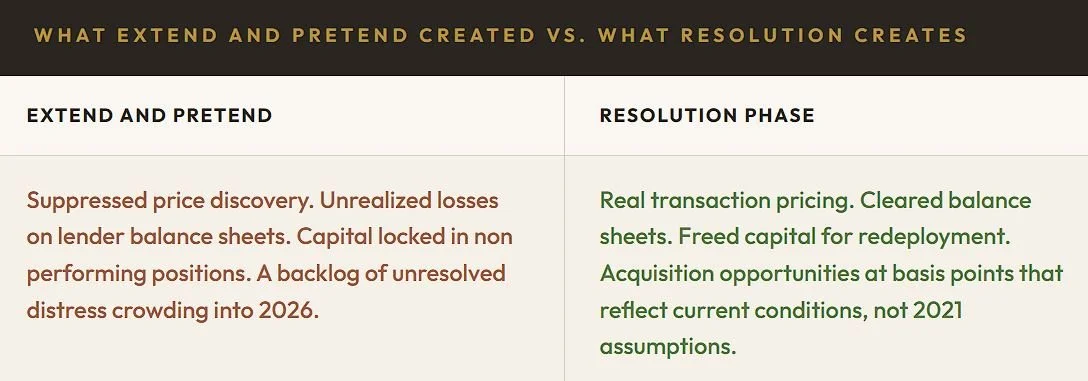

Commercial real estate markets have remained frozen largely because sellers were anchored to yesterday's valuations while buyers underwrote today's financing realities. That disconnect suppressed transaction volume and delayed price discovery across the market.

Forced resolutions change that dynamic. As lenders move distressed assets off their balance sheets, pricing begins reflecting current market conditions rather than prior cycle assumptions. That process creates acquisition opportunities for investors with liquidity, conservative leverage, and long duration capital.

The distinction within the distress cycle also matters.

The strongest investors are not simply asking: where is the distress? They are asking: which distress is temporary, and which is permanent?

Distress Cycles Are Where Long Term Capital Deploys at the Best Basis

Distress cycles are rarely comfortable in real time. But they are often the periods where long term capital is deployed at the most attractive basis.

The end of extend and pretend means the commercial real estate market is finally entering a true price discovery phase after years of delayed resolution. That process will remain uneven. Some assets may never recover prior valuations. Others will transition to stronger ownership structures, cleaner balance sheets, and more sustainable capital stacks.

For sophisticated capital, the opportunity is not in avoiding volatility entirely. It is in understanding where forced selling, refinancing pressure, and market dislocation create asymmetric entry points before broader market sentiment stabilizes.

Four Signals from the Distress Cycle

-

Loan extensions fell from 41% of maturities in 2024 to 21% in 2025. Lenders are forcing resolution through workouts, note sales, and foreclosure rather than granting unconditional time.

-

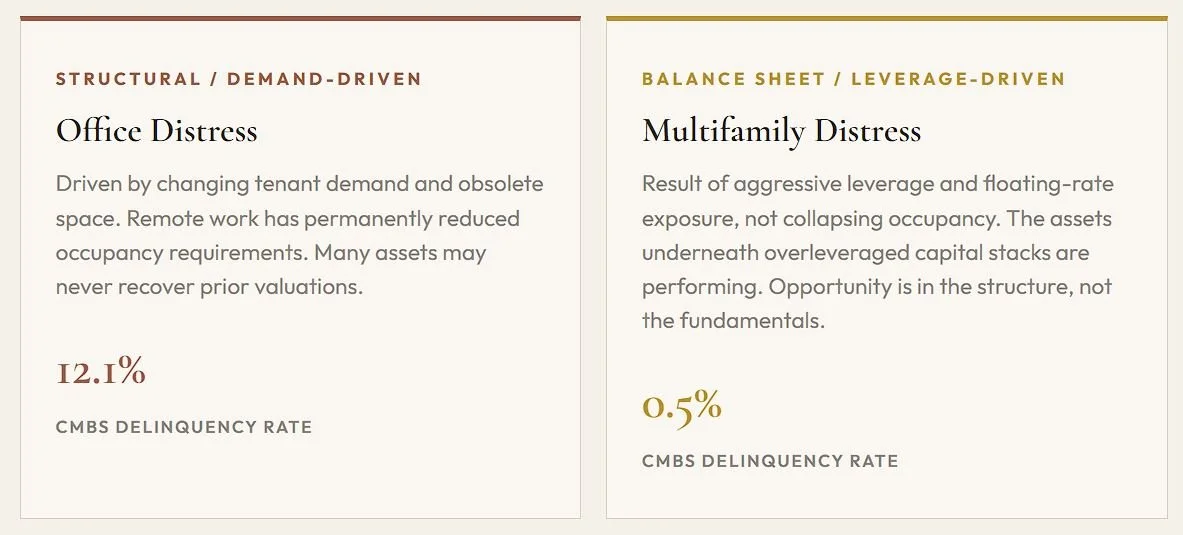

$875 billion matures in 2026. Office CMBS delinquency exceeds 12%. Multifamily CMBS delinquency stands at 0.5%. The distress is concentrated, not systemic.

-

Distressed multifamily sales reached $13.8 billion on a rolling 12-month basis, a 16x increase since 2020. Non performing office notes are clearing at 40 to 60 cents. The bid-ask gap is narrowing.

-

office distress is demand driven. Multifamily distress is leverage driven. The assets underneath overleveraged multifamily capital stacks are performing. The opportunity is in the capital structure, not the fundamentals.

The Best Acquisition Environment in a Decade

“For disciplined allocators, the opportunity is not in avoiding volatility entirely. It is in understanding where forced selling, refinancing pressure, and market dislocation create asymmetric entry points before broader market sentiment stabilizes.”