The Next Housing Bottleneck Is Not Financing. It Is Power.

As AI infrastructure expands, data centers are competing with housing, industrial, and mixed-use developments for the same scarce resource: electricity. The implications reach far beyond technology.

or decades, developers asked one question before buying land: can we build here? Today, a different question matters more: can we power it? That shift is happening faster than most of the real estate market has recognized. And it has implications that extend well beyond data centers into housing development, industrial growth, municipal planning, and long-term capital allocation.

The Scramble for Powered Land

Data center land transactions reached $3.3 billion in Q1 2026, up 141% year over year. But the price being paid is not primarily for the land itself. It is for what sits underneath it: utility connections, substation access, and energized power capacity.

Power as a Strategic Asset

Here is where the story becomes an investment thesis rather than a technology headline.

Power capacity is finite. Substations, transmission lines, and grid interconnections take years to build. When data centers absorb available capacity in a market, every other type of development that requires electricity, including housing, faces a queue. Multifamily builders, industrial developers, and mixed-use projects are increasingly discovering that the utility capacity they assumed would be available has already been committed to hyperscale data center clients willing to pay substantially more for it.

The result is a new form of competition that most real estate investors have not yet priced in. Land with existing power access commands a scarcity premium that is widening every quarter. Sites without it face interconnection timelines measured in years, not months. And the gap between powered and unpowered land values is becoming one of the most significant pricing dynamics in commercial real estate.

“A parcel with utility tie-in capacity is now materially more valuable than an identical parcel without it, regardless of zoning, location, or entitlements. Power access has become the new zoning.”

Why Investors Should Pay Attention

The second-order effects of the power bottleneck are where the investment thesis lives.

-

As data center sponsors bid up powered sites, adjacent land values increase. That cost flows through to every other development type, including workforce housing, where margins are already thin.

-

Utility interconnection queues that once took months now stretch years. Housing developments that depend on new electrical service are being delayed or redesigned to reduce power requirements, adding cost and extending timelines.

-

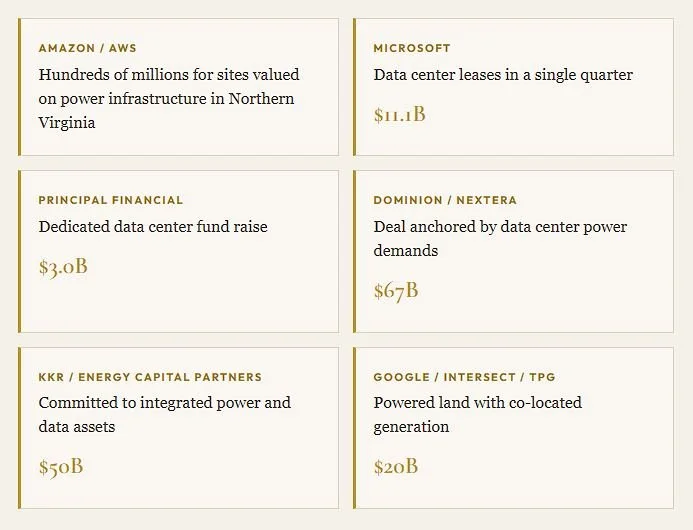

KKR, Energy Capital Partners, Google, Intersect Power, TPG, and Principal Financial are deploying tens of billions into integrated power and data assets. Insurance and pension capital is actively crowding into data center equity. This capital competes directly for the same sites and utility capacity that housing and industrial development require.

-

Dominion Energy proposed its first base-rate increase since 1992 in Virginia. When utilities invest billions to serve data center load, those infrastructure costs are often socialized across all ratepayers, adding to the affordability pressure that workforce renters already face.

“The market often focuses on the buildings people can see. The cranes, the construction sites, the lease announcements. Increasingly, the advantage belongs to the infrastructure most people never think about: the substations, the transmission lines, the utility capacity that determines whether a building can exist at all.”

Where the Barbell Meets the Grid

At IGC, this is not an abstract concern. Our Brightstead Technology partnership provides direct exposure to the digital infrastructure layer where power is the binding constraint. On the housing side, rising utility costs compound the affordability pressure that drives our workforce housing thesis. The power bottleneck does not weaken our positioning. It reinforces both sides of the barbell.

The investors who understand that power access is becoming the most valuable asset in real estate development, not the building, not the location, not even the financing, but the electricity, are the ones who will position most effectively for the next decade.

Jesse Sells

Co-Founder & COO, Impact Growth Capital

The Fourth Constraint

Most investors are still underwriting real estate development around three constraints: financing, construction costs, and demand. Those constraints are real. But a fourth is emerging that may prove more consequential than any of them.

“The next decade of real estate may be shaped less by where growth occurs and more by where power is available.”