The Liquidity Illusion.

Why survival, not returns, may be the most underrated investment strategy in today's market.

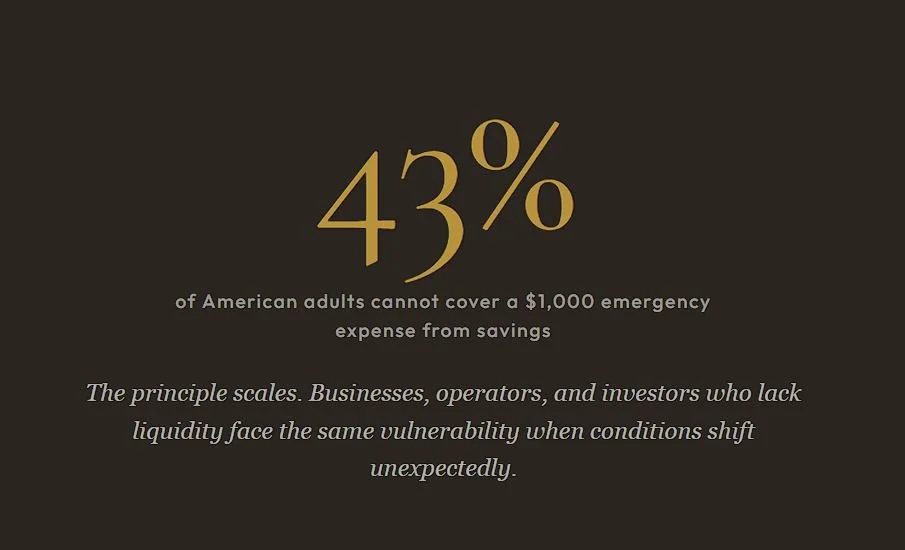

A number crossed my desk this week that stopped me. 43% of American adults cannot cover a $1,000 emergency expense from their savings. The median emergency fund balance has dropped to $5,000, half of what it was a year ago. Investopedia estimates the average household needs roughly $35,000 to cover six months of expenses. The median balance in combined checking and savings accounts is $8,742.

This is not a personal finance newsletter. I am not here to offer savings advice. But that data point illuminates something that applies at every level of capital allocation, from households to family offices to institutional portfolios: liquidity is invisible until it is needed. And by the time it is needed, it is usually too late to create it.

What Most People Misunderstand About Wealth

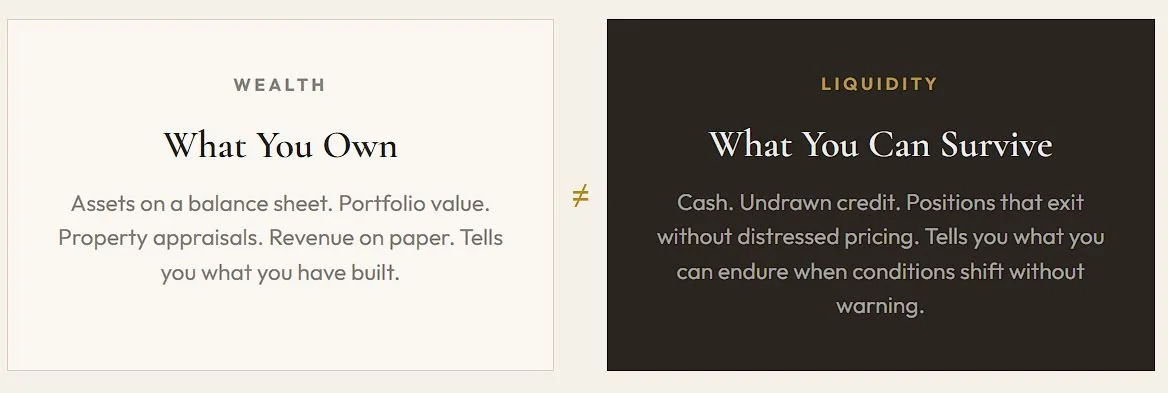

There is a fundamental difference between wealth and liquidity that most investors underestimate. Wealth is what you own. Liquidity is what you can access when conditions change without warning.

A real estate portfolio worth $50 million is wealth. But if the assets cannot be sold, refinanced, or collateralized in a compressed timeline without significant discount, that wealth is not liquid. A business generating $10 million in annual revenue is wealth. But if a supply chain disruption, a regulatory change, or a credit line revocation interrupts cash flow for ninety days, the business can fail despite being profitable on paper.

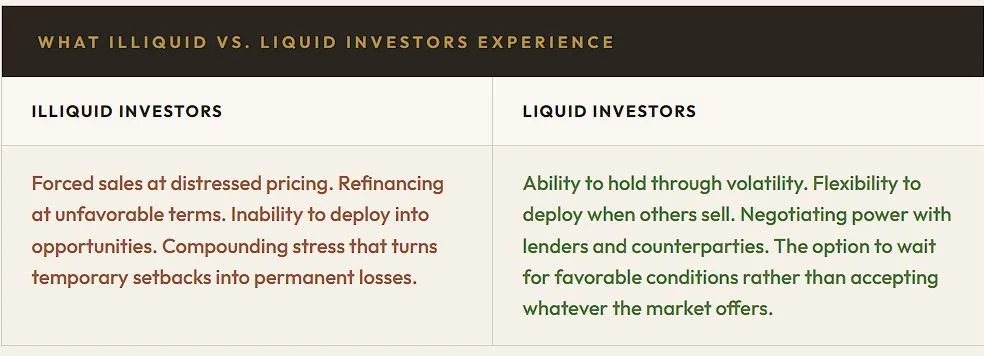

The illusion is that assets on a balance sheet equal options in a crisis. They do not. Options in a crisis come from cash, undrawn credit facilities, and positions that can be exited without accepting distressed pricing. Everything else is a promise that depends on market conditions cooperating at the exact moment you need them to.

Wealth tells you what you have built. Liquidity tells you what you can survive. They are not the same thing. And the difference between them is only visible during stress.

Why Liquidity Matters More Than Investors Realize

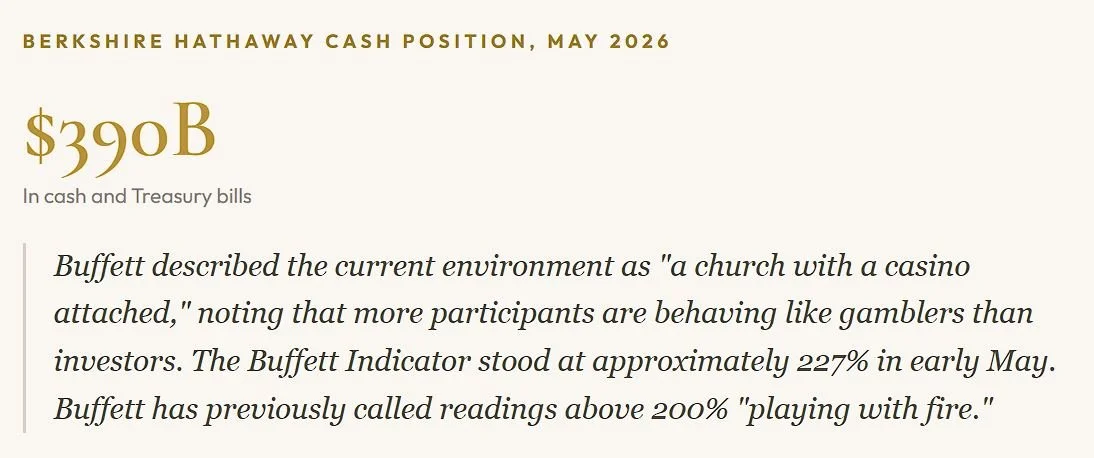

Berkshire Annual Meeting, May 2026. Buffett Indicator = total U.S. market cap / GDP.

Warren Buffett does not hold $390 billion in cash and Treasury bills because he cannot find investments. He holds it because liquidity is optionality. It means that when an opportunity presents itself, whether it is a market dislocation, a forced seller, or an asset repricing, Berkshire can deploy at scale without selling anything else to fund it. That flexibility has been the single most consistent source of Berkshire's outperformance across fifty years and multiple cycles.

The same principle applies at every scale. The real estate operator who maintained conservative leverage and kept reserves is the one who acquires assets from the operator who overleveraged and ran out of time. The family office that held 15% in liquid instruments is the one that deploys into the opportunity that the fully invested family office cannot access.

Lessons from History

Every major financial crisis in modern history has been, at its core, a liquidity crisis. The assets did not disappear. The ability to access capital against them did.

-

Bear Stearns Had Assets. It Did Not Have Liquidity.

The firm was not insolvent on paper. It was illiquid in practice. The same was true for hundreds of real estate operators who owned performing properties but could not refinance when credit markets froze. The buildings were occupied. The rents were being collected. But the loans matured into a market that would not lend, and the assets were sold at discounts that reflected the seller's desperation rather than the asset's value.

-

The Assets Were Not Bad. The Holders Needed Cash.

The March liquidation forced hedge funds, pension plans, and even Treasury markets into forced selling. The assets being sold were not bad. The holders needed cash faster than the market could provide it. Liquidity, not fundamentals, set the price.

-

$875B in CRE Debt Maturing. Extend and Pretend Collapsing.

With $875 billion in CRE debt maturing this year, extend and pretend collapsing, and insurance costs surging 75% in five years, the question is not whether some operators will face liquidity pressure. It is which ones prepared for it and which ones assumed favorable conditions would continue.

What Disciplined Investors Are Doing Differently Today

The SitusAMC data we covered in our last brief showed that 70% of institutional CRE investors now prefer holding cash over deploying. Buy sentiment dropped to 26%. That is not fear. That is discipline. It is capital waiting for clarity before committing to illiquid positions that may take years to unwind if conditions deteriorate further.

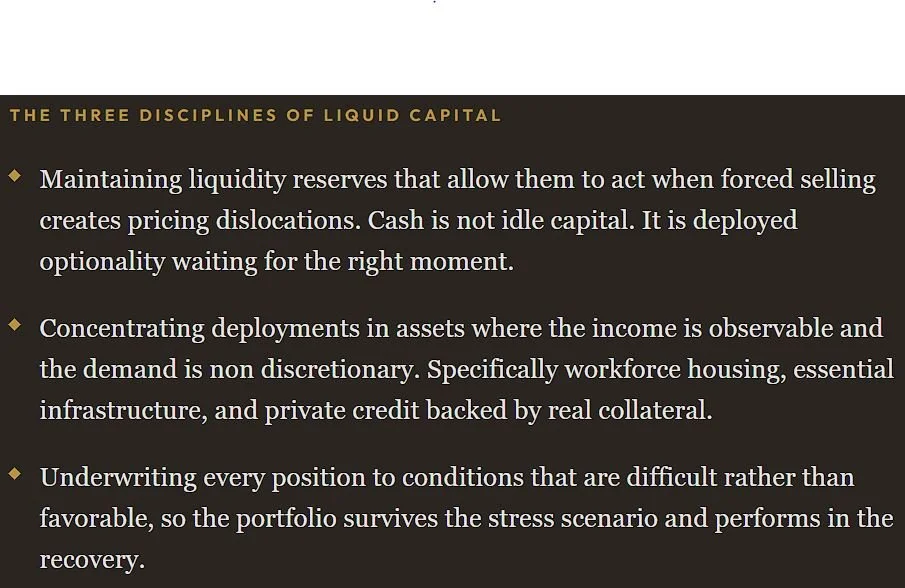

The most disciplined allocators are doing three things simultaneously.

At IGC, this is not a new strategy adopted in response to current conditions. It is the strategy we have always executed. Conservative leverage. Durable income. Essential demand. The barbell holds because both sides generate value in environments where liquidity dependent strategies fail.

The 43% statistic is about households. But the principle scales. It applies to businesses that grew faster than their cash flow could support. To real estate operators who leveraged every dollar of equity into the next deal. To investors who assumed they could always sell at the price they wanted, in the timeframe they needed, in market conditions they expected.

Four Principles of Capital Survival

43% of Americans cannot cover a $1,000 emergency. The principle scales: businesses, operators, and investors who lack liquidity face the same vulnerability when conditions shift unexpectedly.

Wealth is what you own. Liquidity is what you can access. The difference is only visible during stress, which is precisely when it matters most.

Buffett holds $390 billion in cash and Treasuries not because he cannot find investments, but because liquidity is optionality. When others are forced to sell, liquid capital sets the terms.

In investing, the goal is not simply to maximize returns. It is to remain in the game long enough for compounding to do its work. Survival is the strategy that makes every other strategy possible.

The Market Rewards Returns. But It Requires Survival.

Most investors focus on returns. The best investors focus on survival. Not because they are pessimistic, but because they understand that staying in the game is the prerequisite for every return that follows.

“The market rewards returns. But it requires survival. And the distance between those two things is measured in liquidity.”

Jesse Sells

Co-Founder & COO, Impact Growth Capital