When Access Is No Longer the Advantage.

Wall Street is lowering the gates. The question is whether the investors walking through them are prepared for what is on the other side.

This Friday, SpaceX begins trading on the Nasdaq at a targeted valuation of $1.75 trillion. It may become the largest IPO in history. But the valuation is not the most interesting part of the story. What is interesting is how the offering is structured.

SpaceX is reserving up to 30% of shares for retail investors, triple the typical 5% to 10% allocation. Fidelity has reduced its minimum account balance for IPO participation from $100,000 to $500,000 down to just $2,000.

Robinhood requires no minimum at all. Wealthsimple in Canada has launched IPO access with no minimum order size and no fees. For the first time in the history of capital markets, a $1.75 trillion company is essentially inviting everyone to the table.

The question is whether that is an opportunity or a signal.

The Gates Are Open. That Changes the Game.

The SpaceX IPO is the most visible example, but it is not the only one. The entire architecture of investment access has shifted in the last five years. Fractional shares let anyone invest with $1. Alternative investment platforms have lowered private market minimums from $250,000 to $10,000 or less. Crowdfunding regulations expanded. Tokenization is beginning to fractionalize real estate, private credit, and venture exposure.

For decades, access was the advantage. If you could get into a deal, you were ahead. The velvet rope was the edge. Institutional investors outperformed partly because they saw opportunities that retail investors could not reach.

That structural advantage is eroding. Access is being commoditized. And when access is no longer scarce, the advantage shifts to something else entirely.

“When everyone can access the same investments, access stops being the advantage. The advantage becomes what you do after you get in.”

The Second-Order Effects Most Investors Are Missing

Benjamin Felix, chief investment officer at PWL Capital, said it directly in response to the current IPO wave: any time there is a democratization of some exotic product, it is not a good thing for retail investors. That sounds cynical, but the historical data supports it.

When access expands, several dynamics shift simultaneously.

What Changes When Access Expands

-

Institutional allocators who previously received IPO shares conducted extensive due diligence before committing. Many retail participants are making decisions based on brand recognition and social media sentiment.

-

When demand broadens without a corresponding increase in analytical sophistication, assets can be priced at levels that reflect enthusiasm rather than fundamentals.

-

Wall Street analysts are already noting that SpaceX broadening retail allocation to 30% may signal that institutions are pushing back on the $1.75 trillion valuation.

This is not a statement about SpaceX specifically. It is a principle that applies across every asset class where access is expanding: when the gates open wider, the question to ask is not whether you can get in. It is whether the terms at which you are getting in still make sense.

What This Means for Investors Over the Next Decade

The commoditization of access is permanent. It will not reverse. Over the next five to ten years, retail investors will have entry into virtually every asset class that was once institutional-only: private equity, venture capital, private credit, real estate funds, and infrastructure.

The regulatory trajectory, the technology trajectory, and the competitive dynamics among platforms all point in one direction. That means the investor who thrives in the next decade will not be the one with the best access.

It will be the one with the best process.

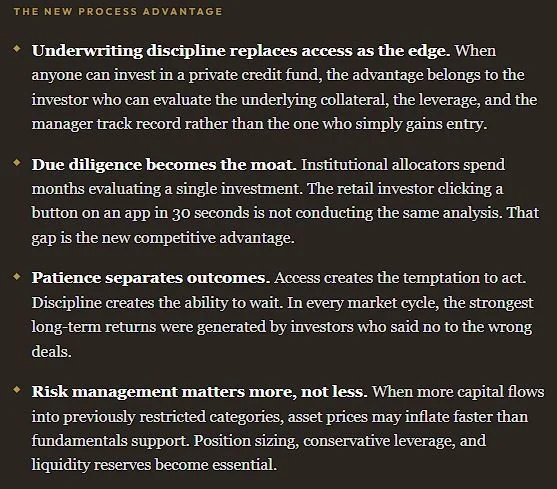

Access Is Not the Strategy. Discipline Is.

At IGC, we have never competed on access. We compete on underwriting. On due diligence. On conservative leverage and structural demand. On the discipline to deploy only when the math works and to hold liquidity when it does not.

The SpaceX IPO is exciting. The democratization of investment is, in many ways, a positive development. But excitement and access are not substitutes for analysis. The investors who will build durable wealth over the next decade are not the ones who get into the most deals.

They are the ones who get into the right deals at the right terms with the right structure. That has always been the advantage. It just matters more now that everyone else is in the room.

Four Principles for the New Access Era

Access is being commoditized. Fidelity dropped IPO minimums from $100K+ to $2,000. SpaceX is reserving 30% for retail versus the typical 5% to 10%. The velvet rope is disappearing across every asset class.

When access is no longer scarce, the advantage shifts to underwriting, due diligence, risk management, and patience. These are the disciplines that separate durable wealth from participation.

Expanded access changes pricing dynamics. When demand broadens without a corresponding increase in analytical sophistication, assets can be priced at levels that reflect enthusiasm rather than fundamentals.

The investors who build durable wealth over the next decade will not be the ones who get into the most deals. They will be the ones who get into the right deals at the right terms with the right structure.

The Best Investors Know Which Deals to Walk Away From.

The gates are open. More investors can participate in more asset classes than at any point in financial history. That is, in many ways, progress.

But access without discipline is exposure without protection. The advantage now belongs to the investors who treat every opportunity, no matter how exciting, with the same rigor: what is the underlying value, what are the risks, what is the exit, and does the math work at the terms being offered?