Higher for Longer, But the Barbell Holds.

The April FOMC minutes confirm the Fed is not ready to cut. Nvidia's $75 billion data center quarter validates infrastructure demand. Multifamily rent data shows durable ballast. In this regime, asset selection matters more than rate predictions. The barbell still makes sense.

The April FOMC minutes, released Wednesday, reinforced a message markets have been resisting for months: the Federal Reserve is not yet convinced inflation is contained, and rate cuts are not imminent. That matters because for allocators in hard assets, the difference between a soft cut narrative and a higher for longer regime is not semantic. It changes underwriting, refinancing assumptions, cap rate discipline, and where growth risk can be taken with confidence.

What makes this week's read different from every other "Fed stays restrictive" take is the leadership turnover sitting underneath the data. These minutes are from Powell's last meeting. Four officials dissented. Kevin Warsh was confirmed as Fed Chair on May 13 and runs his first FOMC on June 16 to 17. Markets are not just digesting hot inflation prints. They are pricing a new chair, inheriting a divided committee, with the inflation data running the wrong way going into his first decision.

The most important implication is not simply that capital stays more expensive for longer. It is that asset selection matters more. When the risk free rate refuses to cooperate, investors need income that can hold up without aggressive assumptions and growth that is strong enough to outrun a high discount rate.

Hot Inflation Into a Leadership Transition

Minutes from the April 28 to 29 FOMC meeting show a committee increasingly uneasy with the recent inflation data and more willing to contemplate tighter policy if price pressures do not moderate. The release follows a hot April producer price report.

Sharpest monthly PPI gain since March 2022. Energy shock layered on reaccelerating core.

The shape of that inflation print matters. Roughly three quarters of the surprise came from energy, with final demand energy up 7.8 percent and gasoline up 15.6 percent, tied to Middle East developments the Fed itself has flagged. But core PPI also ran 1.0 percent month over month, the hottest core print since March 2022. That combination, an energy shock layered on top of reaccelerating core, is the worst possible setup for a Fed inheriting a new chair.

It is precisely the kind of inflation rate policy cannot easily fix, which is why "higher for longer" is now the more honest base case.

“For private capital, that means resisting the temptation to underwrite a friendlier cost of capital environment just a quarter or two out. In this regime, the spread between disciplined and optimistic underwriting widens quickly.”

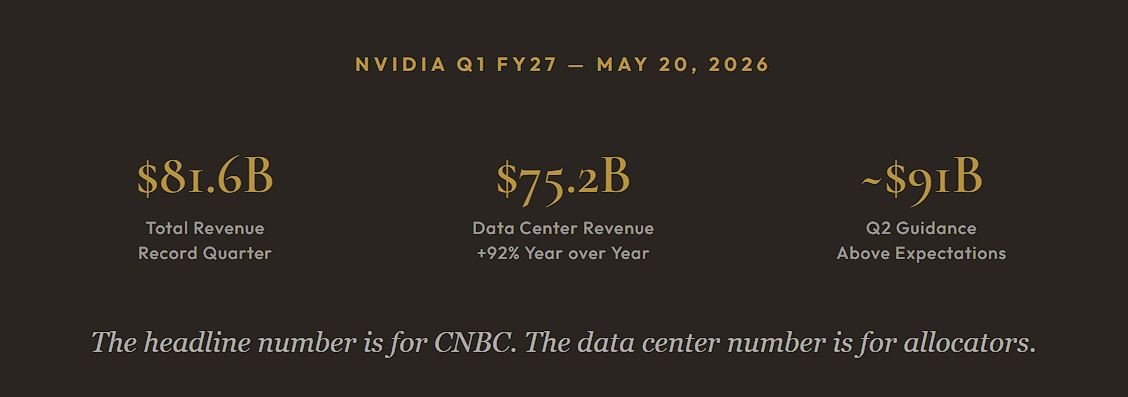

What Nvidia's Quarter Tells Allocators

That is what makes Nvidia's earnings report so instructive. Data center revenue at $75.2 billion in a single quarter, growing 92 percent annually, is the bottleneck story expressed in dollars. This is not a speculative future theme. It is a current capex cycle with measurable urgency behind it.

The significance for private capital is not about chasing public market momentum. It is that even in a higher for longer environment, capital will still reward growth when the underlying demand is visible, structural, and capacity constrained. Plenty of long duration growth assets struggle when rates stay elevated. AI infrastructure appears to be one of the few areas where demand is strong enough to absorb that pressure.

This is where the upside side of the barbell earns its place. Data centers, powered land, interconnection capacity, and associated infrastructure sit closer to the real bottlenecks than the headline equity story does. Public markets price the chips first. Private capital has an opportunity further down the stack, where physical infrastructure remains scarce and increasingly essential.

Soft Rents Do Not Mean Broken Fundamentals

On the defensive side, the latest Yardi Matrix national multifamily report showed modest nominal rent growth in April, with average asking rents up just $4 to $1,758, down 0.2 percent year over year, with year to date growth at 0.4 percent, roughly one third of the 2012 to 2019 seasonal norm.

But the national number hides what is actually happening on the ground.

Source: Yardi Matrix National Multifamily Report, April 2026. Year over year asking rent growth.

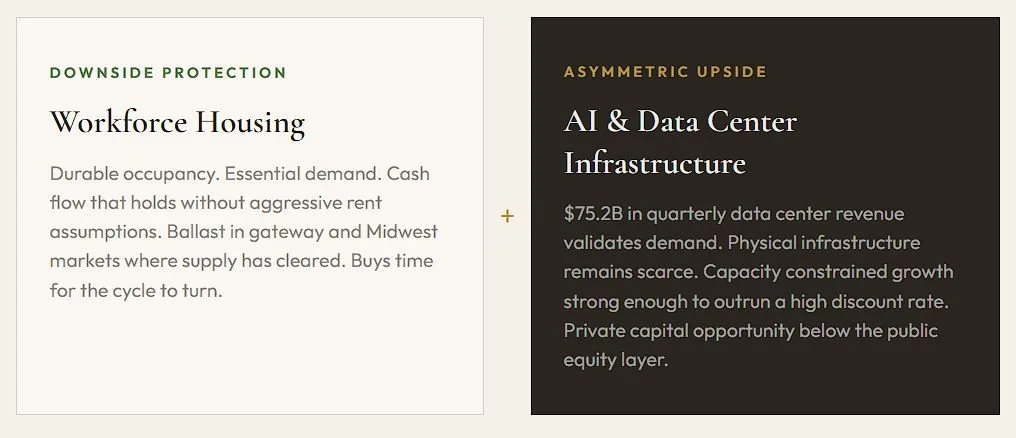

Workforce housing as ballast is the right call, but ballast in a gateway or Midwest market is doing very different work than ballast in a Sun Belt market still digesting supply.

In a market where financing costs remain elevated and inflation has not fully normalized, the value of workforce housing is not in heroic rent assumptions. It is in durable occupancy, essential demand, and cash flow that can remain resilient without depending on capital markets generosity. The wrong conclusion from soft real rent growth is that housing is broken. The better conclusion is that stabilized, well located housing should be underwritten as ballast, not as venture capital.

“If the Fed is telling investors that financing conditions may stay restrictive, then the assets that deserve premium attention are the ones that can hold value through slower rent growth, tighter debt markets, and a longer wait for cap rate relief.”

Pair Downside Protection with Asymmetric Upside

The macro message from this week is straightforward. The Fed is keeping pressure on the system longer than markets hoped, and the chair handover into June makes any dovish pivot harder to underwrite. Nvidia's quarter shows that some forms of infrastructure led growth are still powerful enough to compound through that pressure. Multifamily data shows that income producing housing is not a high growth story today, but it remains a durable one, especially in markets where supply has cleared.

That is the portfolio construction lesson. In this environment, the smartest posture is not to swing entirely defensive or entirely cyclical. It is to pair downside protection with asymmetrical upside. The cash flow durability of well located workforce housing buys time. AI and data center infrastructure offers exposure to one of the few demand cycles strong enough to justify large scale capital deployment despite a stubbornly high cost of money.

Three Data Points That Shape the Near Term Tape

-

April PCE release. A hot print confirms the PPI signal and pushes any cut conversation deeper into 2026.

-

May nonfarm payrolls. A soft jobs print reopens the cut door but raises a different problem for growth assumptions in real estate.

-

Warsh's first FOMC. The June 17 statement, however brief, will be the first real read on what the new Fed actually intends to do.

Closing Perspective

Underwrite to the Regime in Front of Us

For now, the posture has not changed. Underwrite to the rate regime in front of us, not the one markets keep wishing for. Pair real income with real growth.

“The barbell holds. Workforce housing buys time. AI infrastructure earns the multiple. In a higher for longer world, that combination is not just defensible. It is the clearest expression of disciplined capital allocation available.”